In the United States today, you can have your bank account closed, your credit cards cancelled, and your online payments revoked for any number of crimes, like funding terrorism, engaging in money laundering, or violating sanctions.

Sensible, right? Well, you can also face financial ruin for teaching poetry.

That’s what seemingly happened to a Persian poetry teacher from Detroit whose accounts were flagged for “sanctions violations” because his students wrote “Persian classes” in their Venmo memos. There’s also the story about the naked yoga practitioners who lost their payment processor for 60 days, forced to rebuild a subscriber list from scratch. And we can’t forget the San Diego cannabis journalist cut off from Stripe—and from a paid Substack newsletter—because of the payment platform’s rules that prohibit the promotion of the sale of cannabis.

This is “financial censorship,” and it often happens when a bank, credit card provider, or payment app decides that a customer is too risky to serve. But “risky” doesn’t always mean “illegal,” and when a major financial institution errs towards caution about what a customer is saying, advocating for, representing, or publishing, a lot of innocent people can be hurt in the process.

That’s what the digital rights activist Rainey Reitman learned in writing “Transaction Denied: Big Finance’s Power to Punish Speech.” As Reitman explained about these hugely impactful decisions:

“Even if they are well-intentioned, the financial systems can end up pulling in a lot of people that are not the actual target… Sometimes we talk about this as dolphins in the fishing lines.”

These decisions are difficult to fight, frustratingly opaque, and nearly impossible to reverse. Compounding the problem is that that there aren’t enough alternatives available for the financially censored to easily regain their freedom.

The reality for hundreds of millions of people in this country is that about a dozen companies control all their finances. People mostly bank with Chase, or Bank of America, or Citigroup, or Wells Fargo. They mostly use credit cards assigned by Visa, MasterCard, American Express, or Capital One. And they mostly send money to one another and to small businesses using services like PayPal, Venmo, Cash app, and Square.

For most people, these companies are supposed to operate in the background of their lives, providing reliable, secure financing to sustain and manage their livelihoods. But in practice, these companies can become quite interested in what you say online, what payments you receive each month, and the locations those payments arrived from.

Today, on the Lock and Code podcast with host David Ruiz, we speak with Reitman—who is also the president and a co-founder of the Freedom of the Press Foundation—about the real stories of those who have been financially censored, why financial companies cut off customers for legal speech, and how a single company’s decision can create cascading consequences that feel impossible to fight.

“They’d be locked out of Venmo, then they’d be locked out of PayPal—which is connected to Venmo—and then they’d suddenly lose their Chase Bank account. You could see that in a lot of instances, losing one form of access to the financial system, it could result in a pattern where they would be losing access repeatedly.”

In those cases, scammers created a PayPal subscription and then paused it, which triggered PayPal’s genuine “Your automatic payment is no longer active” notification. They also set up a fake subscriber account, likely a Google Workspace mailing list, which automatically forwarded any email it received to all other group members.

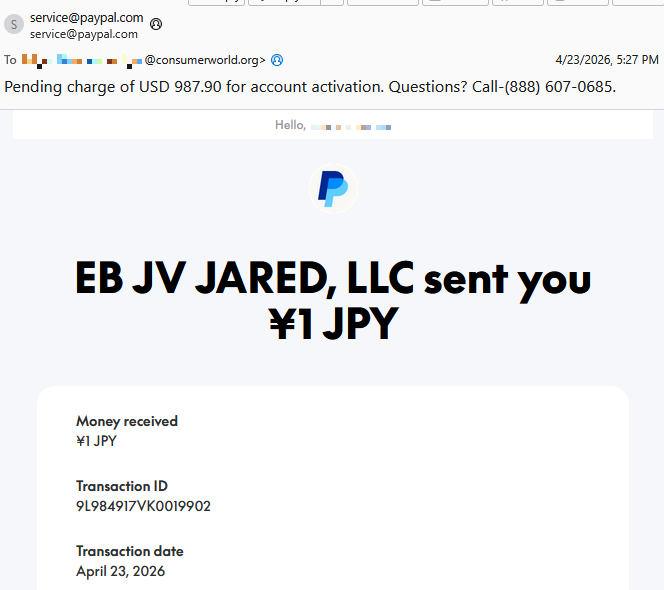

Recently, ConsumerWorld.org alerted us that tech support scammers have found a way to manipulate the subject line of PayPal payment notifications.

This is a screenshot of the example they sent us.

Screenshot email from PayPal scammers

As you can see, the email comes from service@paypal.com. It wasn’t spoofed, which means it passes standard security checks (DKIM, SPF, DMARC).

While the body of the email says that you received a payment of ¥1 JPY (a whopping $0.0063), the subject line tells a different story:

“Pending charge of USD 987.90 for account activation. Questions? Call-(888) 607-0685.”

As an extra bonus for the scammers, the email contains personalized details—the recipient’s actual name and a real transaction ID.

The number in the subject line is not PayPal’s. The legitimate contact number appears inside the email.

“The amount doesn’t match what I see in the email body—that’s weird and scary.”

“I need to call this number immediately to dispute this charge.”

They call the number in the subject line, only to reach tech support scammers.

These scammers pretend to be PayPal support and may try to:

Get you to “verify” payment methods

Collect banking details

Convince you to install remote access tools

Take control of accounts or devices

All of the above

How the subject line is altered is still unclear. Based on PayPal’s documented email behavior, subject lines are typically fixed and not meant to include arbitrary free text or phone numbers. Our findings indicate that the subject line was already weaponized at the point PayPal’s systems signed the email. If someone along the way had rewritten the subject, the dkim=pass header.d=paypal.com result would likely fail.

One possibility is that the scammer abused PayPal’s note or remittance field in a way that surfaces in certain payout templates, including the subject line and HTML <title>, even though normal merchant payment‑received emails don’t allow arbitrary subjects.

The title tag matches the subject line of the email

We have contacted PayPal for comment and will update this post if we hear back.

How to avoid PayPal scams

The best way to stay safe is to stay informed about the tricks scammers use. Learn to spot the red flags that almost always give away scams and phishing emails, and remember:

Use verified, official ways to contact companies. Don’t call numbers listed in suspicious emails or attachments.

Beware of someone wanting to connect to your computer remotely. One of the tech support scammer’s biggest weapons is their ability to connect remotely to their victims. If they do this, they essentially have total access to all of your files and folders.

Report suspicious emails to PayPal.Send the email to phishing@paypal.com to support their investigations.

If you’ve fallen victim to a tech support scam:

Paid the scammer? Contact your bank or card provider and let them know what’s happened. You can also file a complaint with the FTC or your local law enforcement, depending on your region.

Shared a password? Change it anywhere it’s used. Consider using a password manager and enable 2FA for important accounts.

Gave access to your device?Run a full security scan. If scammers had access to your system, they may have planted a backdoor so they can revisit whenever they feel like it. Malwarebytes can remove these and other software left behind by scammers.

Watch your accounts: Keep an eye out for unexpected payments or suspicious charges on your credit cards and bank accounts.

Be wary of suspicious emails. If you’ve fallen for one scam, they may target you again.

Pro tip: Malwarebytes Scam Guard recognized this email as a call back scam. Upload any suspicious text, emails, attachments, and other files to ask for its opinion. It’s really very good at recognizing scams.

Something feel off? Check it before you click.

Malwarebytes Scam Guard helps you analyze suspicious links, texts, and screenshots instantly.

In 2025, the financial cyberthreat landscape continued to evolve. While traditional PC banking malware declined in relative prevalence, this shift was offset by the rapid growth of credential theft by infostealers. Attackers increasingly relied on aggregation and reuse of stolen data, rather than developing entirely new malware capabilities.

To describe the financial threat landscape in 2025, we analyzed anonymized data on malicious activities detected on the devices of Kaspersky security product users and consensually provided to us through the Kaspersky Security Network (KSN), along with publicly available data and data on the dark web.

We analyzed the data for

financial phishing,

banking malware,

infostealers and the dark web.

Key findings

Phishing

Phishing activity in 2025 shifted toward e-commerce (14.17%) and digital services (16.15%), with attackers increasingly tailoring campaigns to regional trends and user behavior, making social engineering more targeted despite reduced focus on traditional banking lures.

Banking malware

Financial PC malware declined in prevalence but remained a persistent threat, with established families continuing to operate, while attackers increasingly prioritize credential access and indirect fraud over deploying complex banking Trojans. To the contrary, mobile banking malware continues growing, as we wrote in detail in our mobile malware report.

Infostealers and the dark web

Infostealers became a central driver of financial cybercrime, fueling a growing dark web economy where stolen credentials, payment data, and full identity profiles are traded at scale, enabling widespread and destructive fraud operations.

Financial phishing

In 2025, online fraudsters continued to lure users to phishing and scam pages that mimicked the websites of popular brands and financial organizations. Attackers leveraged increasingly convincing social engineering techniques and brand impersonation to exploit user trust. Rather than relying solely on volume, campaigns showed greater targeting and contextual adaptation, reflecting a maturation of phishing operations.

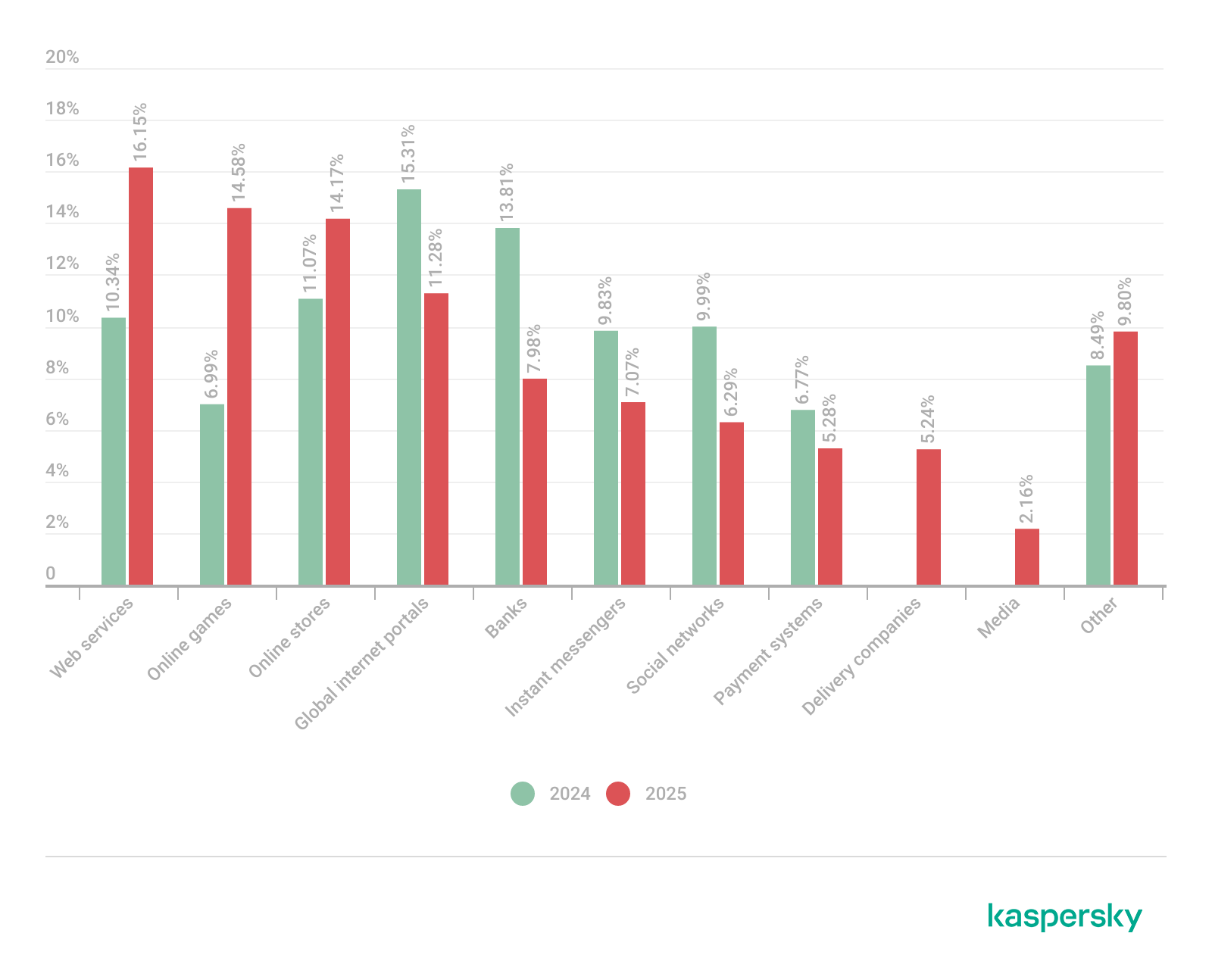

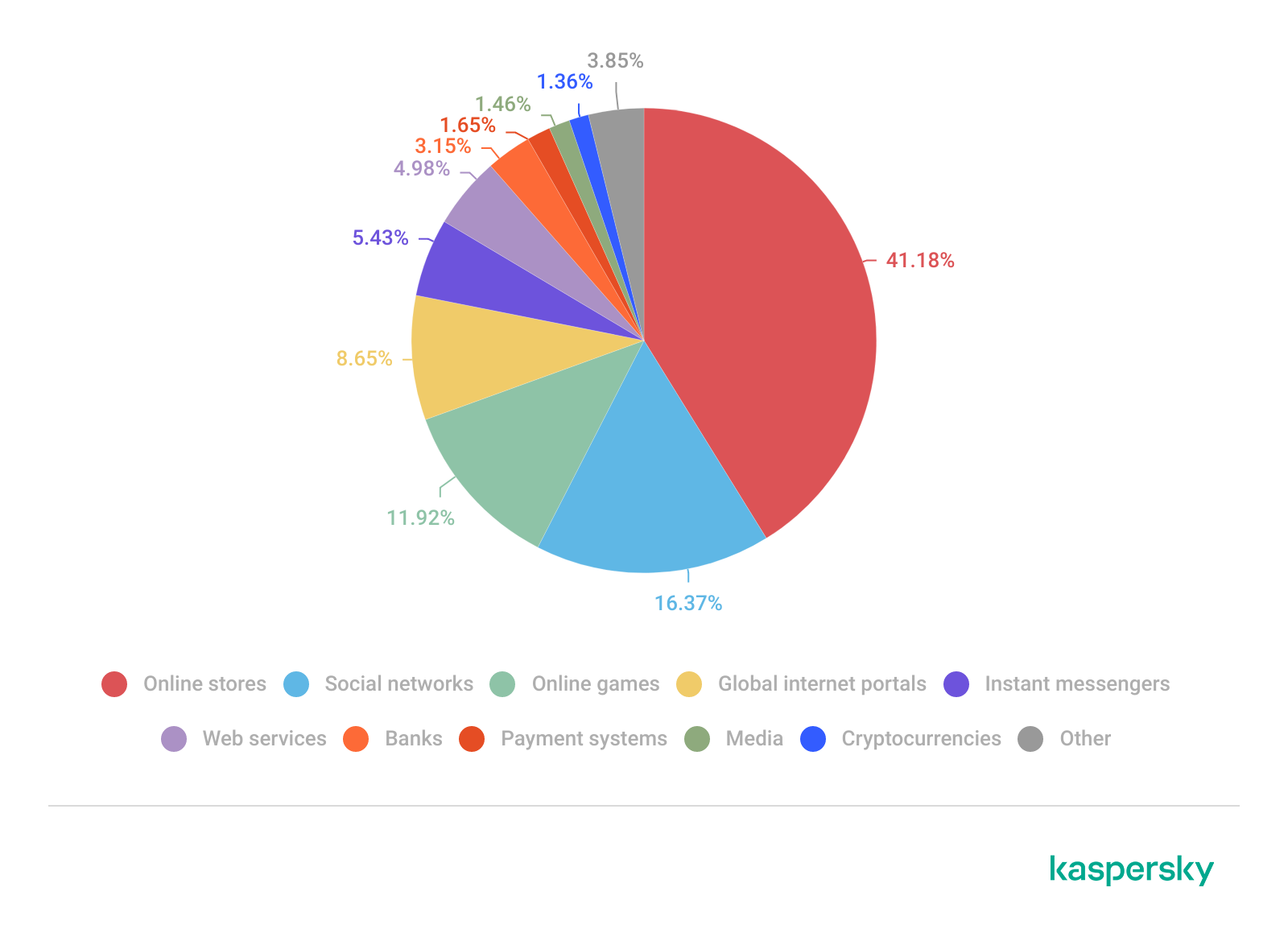

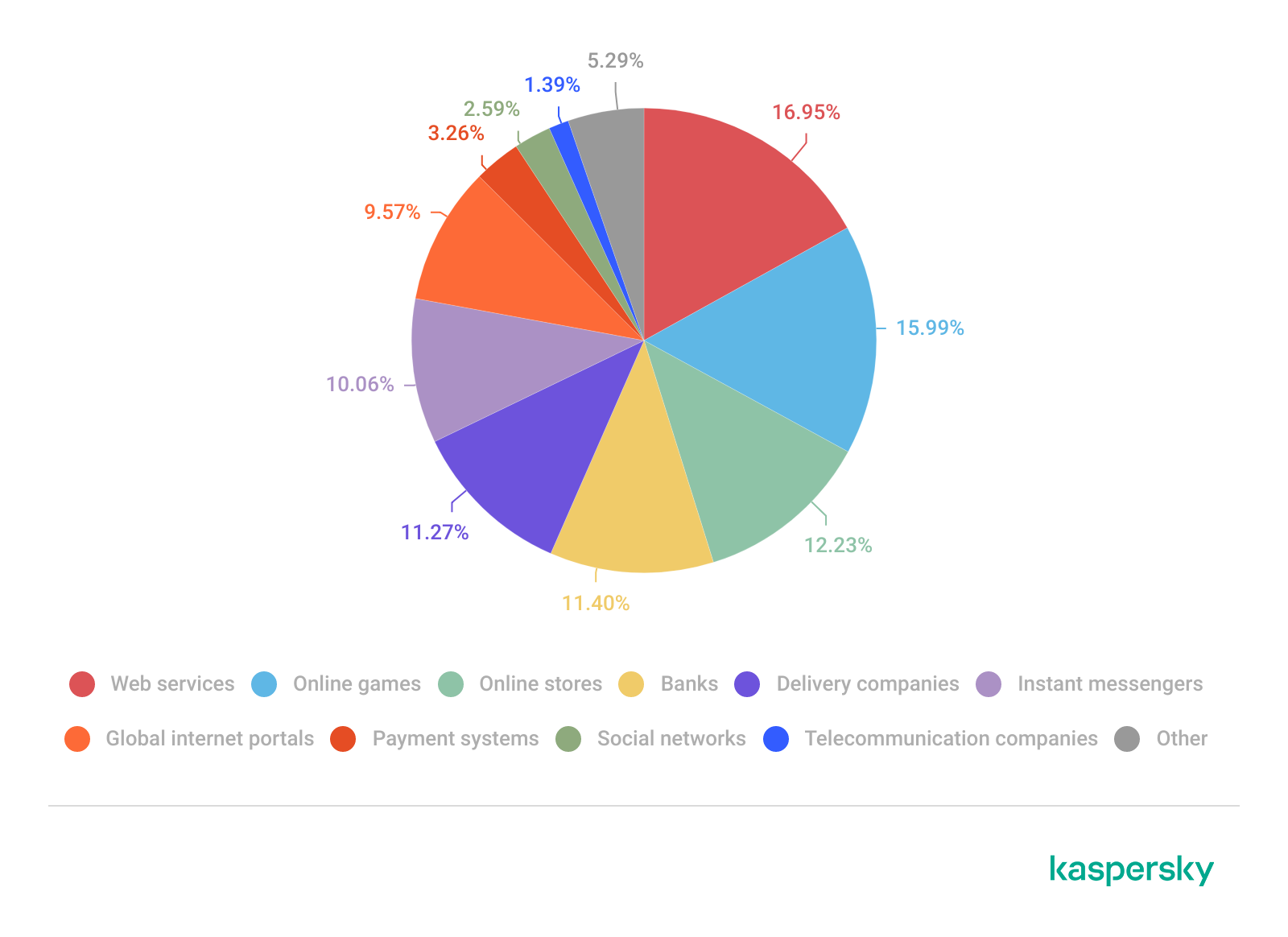

The distribution of top phishing categories in 2025 shows a clear shift toward digital platforms that aggregate multiple user activities, with web services (16.15%), online games (14.58%), and online stores (14.17%) leading globally. Compared to 2024, the rise of online games and the decline of social networks and banks indicate that attackers are increasingly targeting environments where users are more likely to take a risk or engage impulsively. Categories such as instant messaging apps and global internet portals remain significant phishing targets, reflecting their role as communication and access hubs that can be exploited for credential harvesting.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices, 2025 (download)

Regional patterns further reinforce the adaptive nature of phishing campaigns, showing that attackers closely align category targeting with local digital habits. For example, online stores dominate heavily in the Middle East.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in the Middle East, 2025 (download)

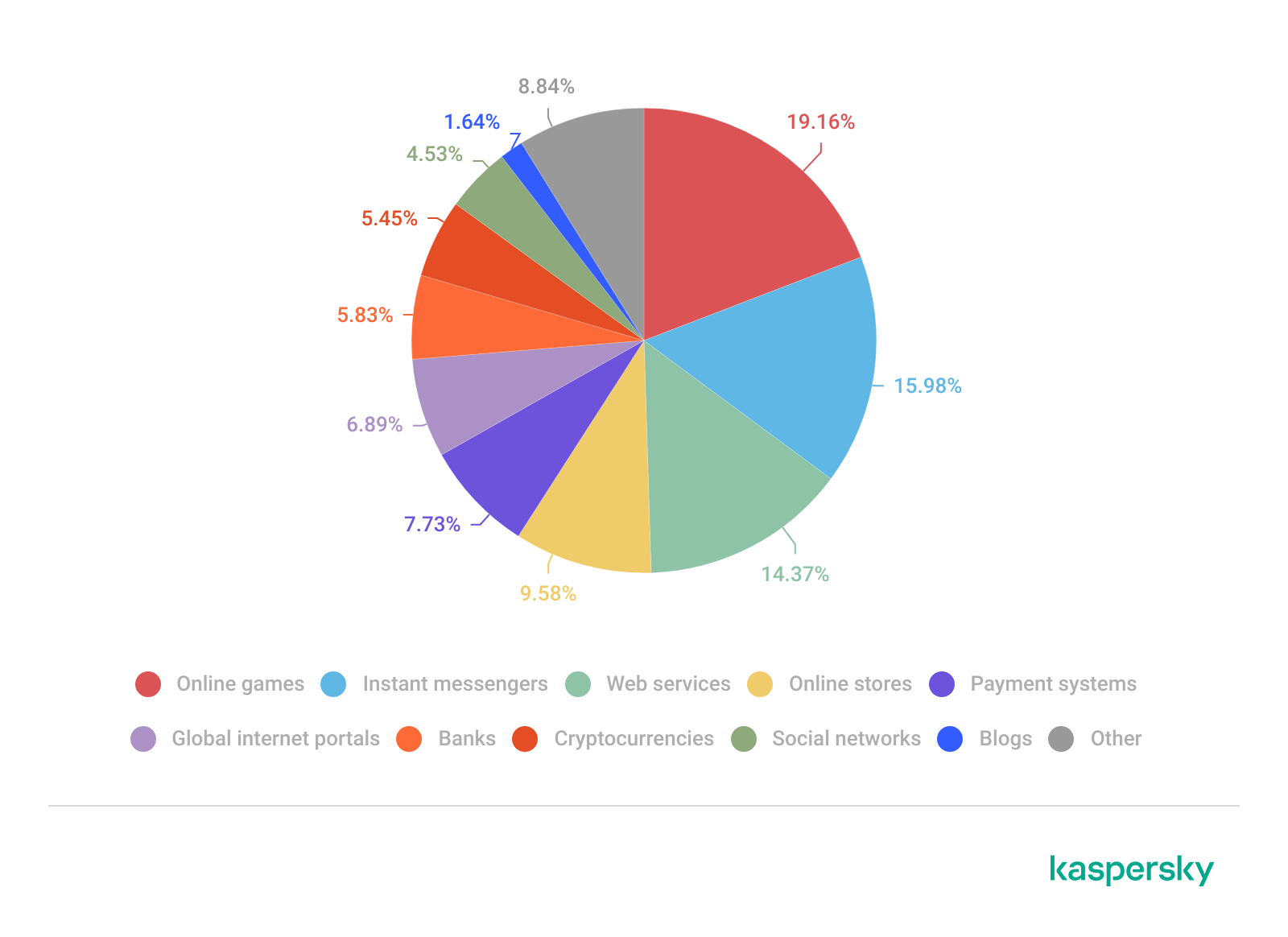

Online games and instant messaging platforms feature more prominently in the CIS, suggesting a focus on younger or highly connected user bases.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in the CIS, 2025 (download)

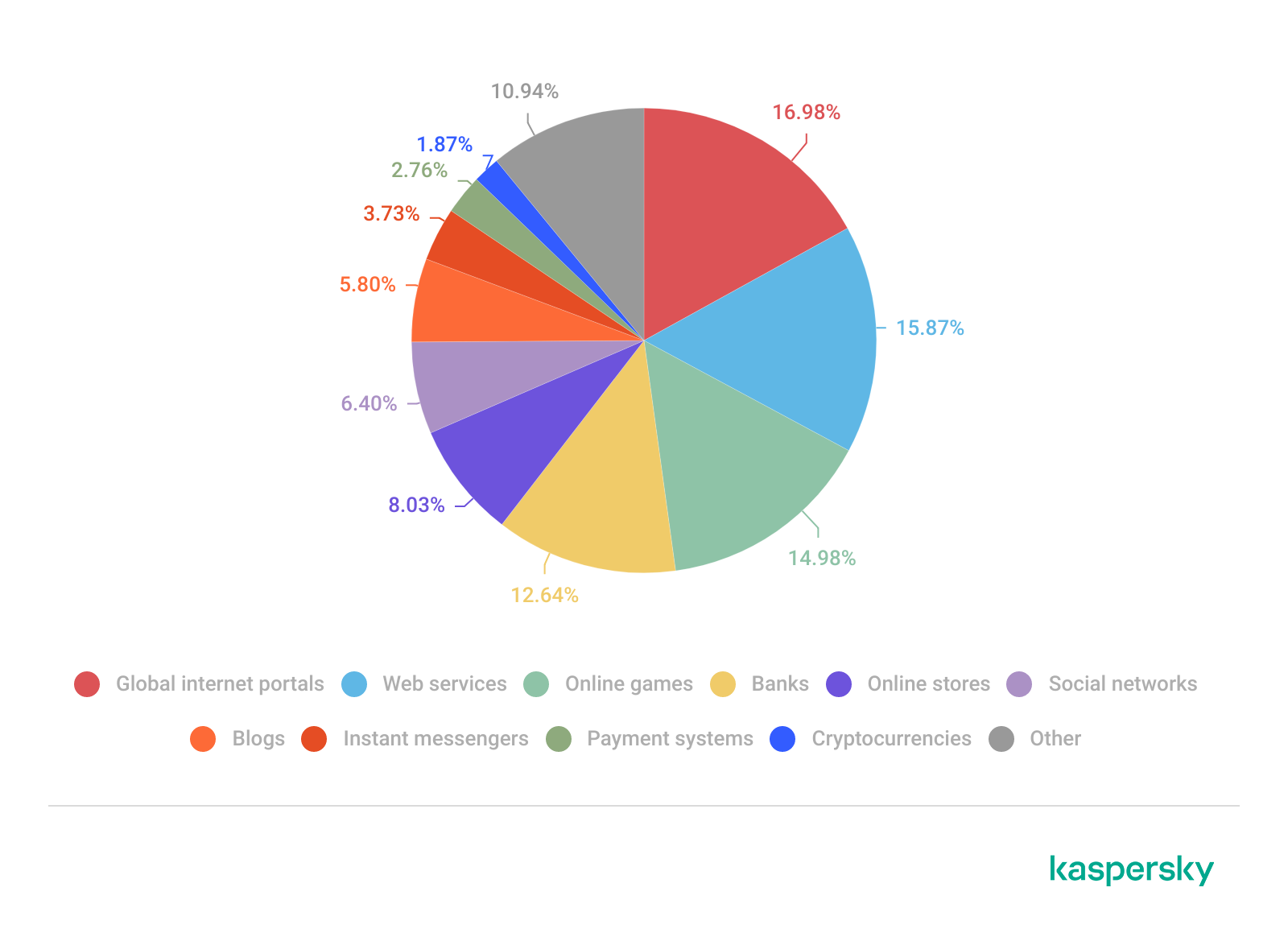

APAC demonstrates almost equal shares of online games and banks which signifies a combined approach targeting different users.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in APAC, 2025 (download)

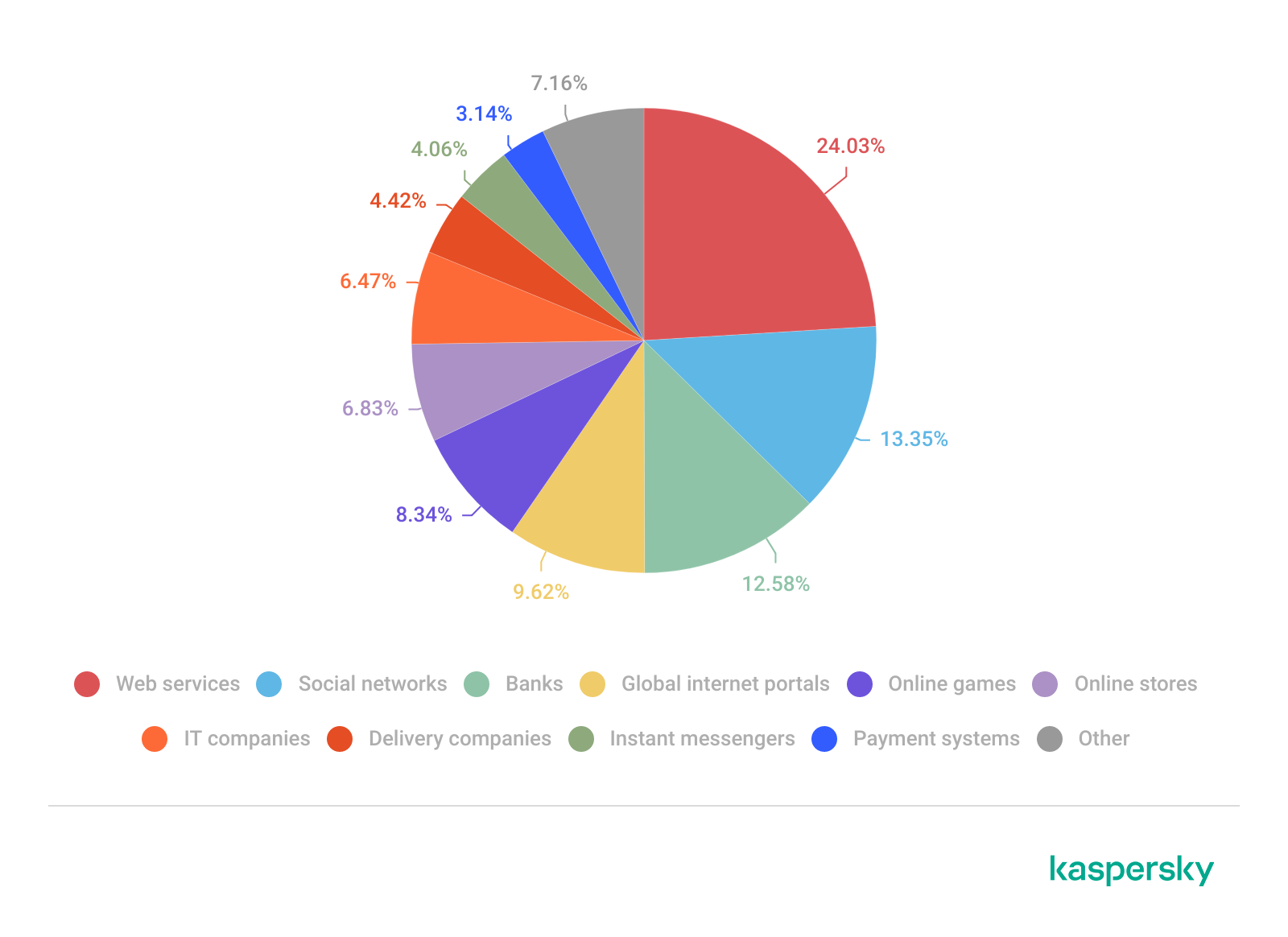

In Africa, a stronger emphasis on banks reflects the continued importance of traditional financial services. Most likely, this is due to the lower security level of the financial institutions in the region.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in Africa, 2025 (download)

Whereas in LATAM, delivery companies appearing in the top categories indicate attackers exploiting the growth of e-commerce logistics.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in Latin America, 2025 (download)

Europe presents a more balanced distribution across categories, pointing to diversified attack strategies.

TOP 10 categories of organizations mimicked by phishing and scam pages that were blocked on home users’ devices in Europe, 2025 (download)

Attackers actively localize their tactics to maximize relevance and effectiveness.

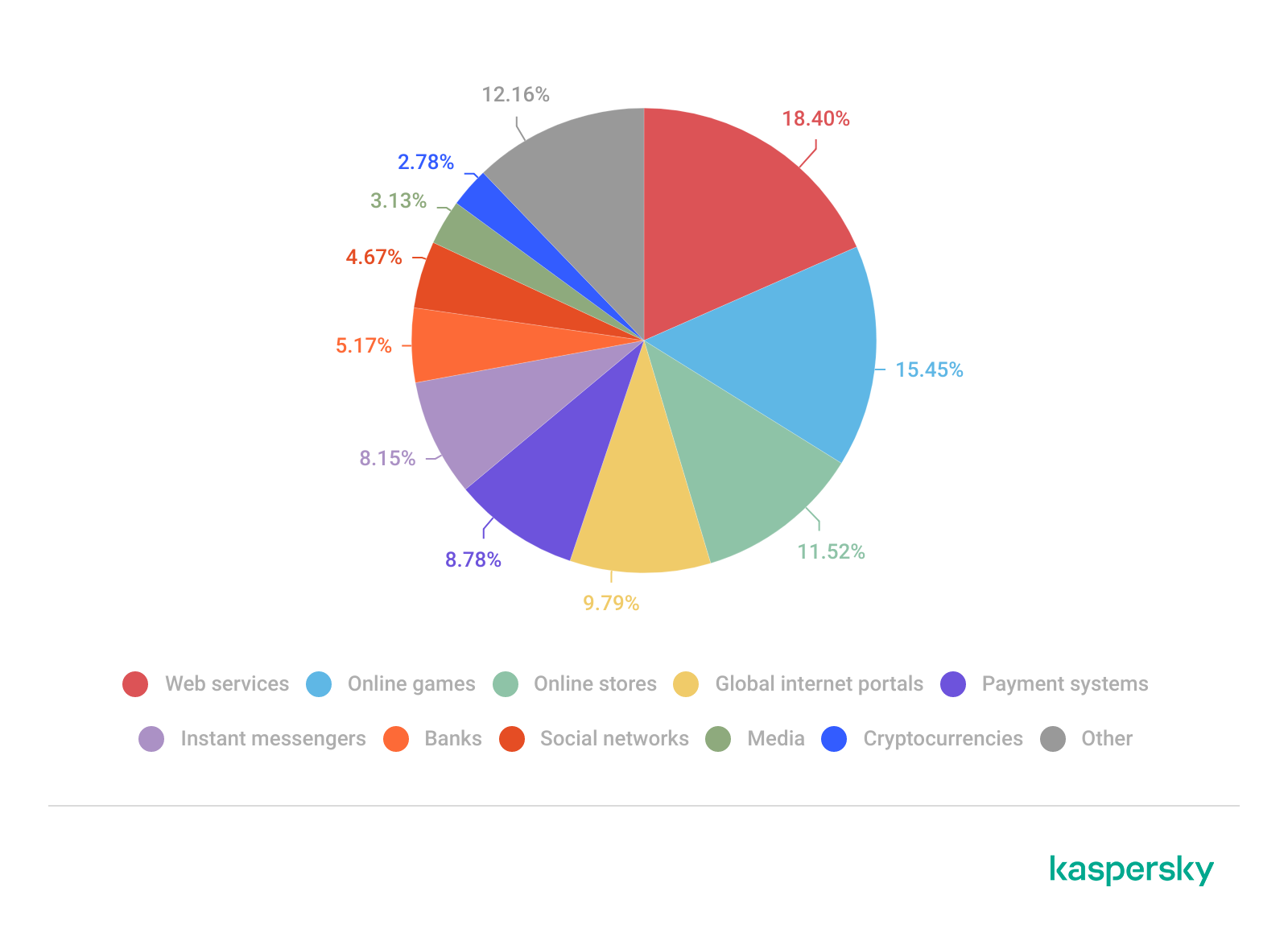

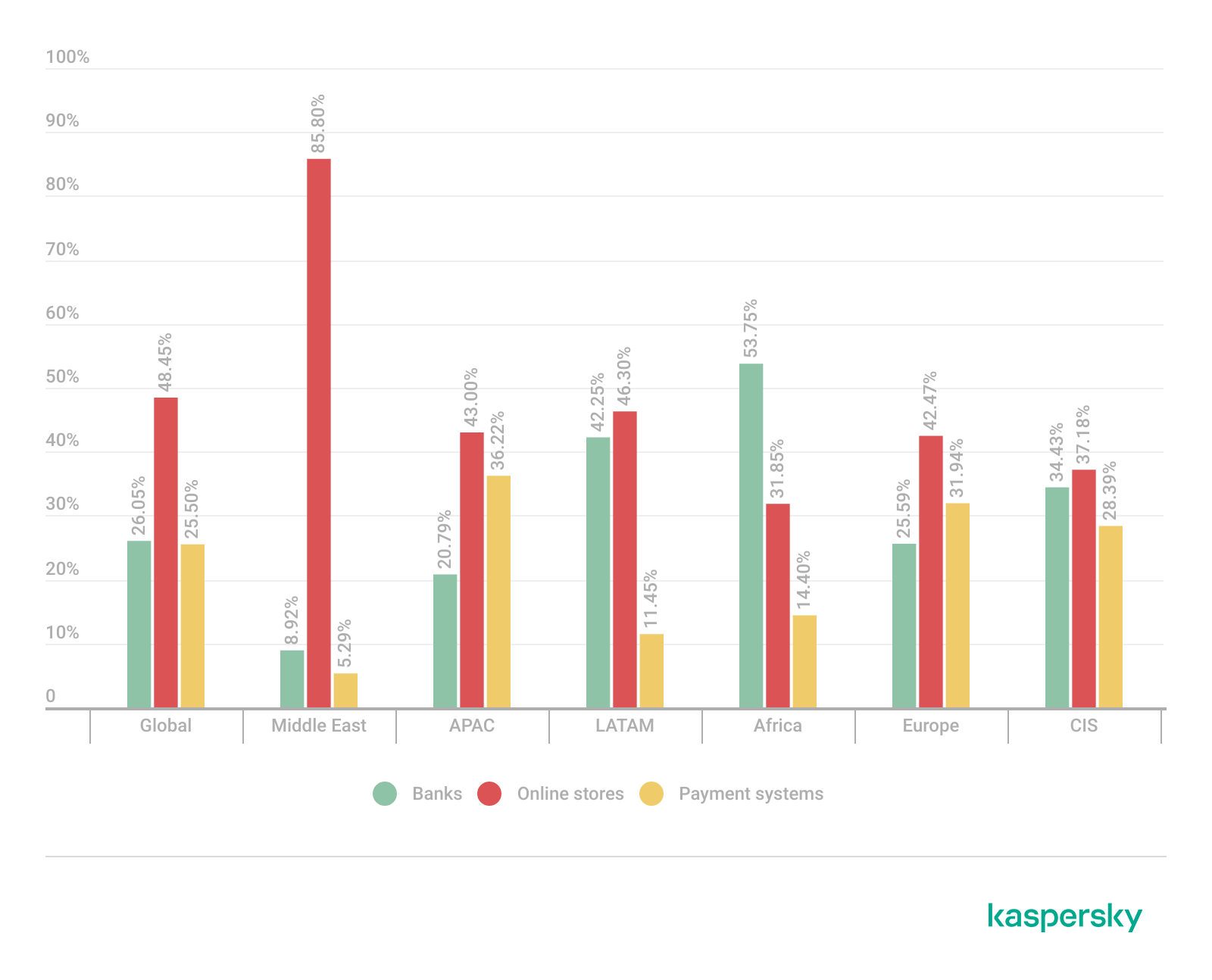

The distribution of financial phishing pages by category in 2025 reveals strong regional asymmetries that reflect both user behavior and attacker prioritization.

Globally, online stores dominated (48.45%), followed by banks (26.05%) and payment systems (25.50%). The decline in bank phishing may suggest that these services are becoming increasingly difficult to successfully impersonate, so fraudsters are turning to easier ways to access users’ finances.

However, this balance shifts significantly at the regional level.

In the Middle East, phishing is overwhelmingly concentrated on e-commerce (85.8%), indicating a heavy reliance on online retail lures, whereas in Africa, bank-related phishing leads (53.75%), which may indicate that user account security there is still insufficient. LATAM shows a more balanced distribution but with a higher share of online store targeting (46.30%), while APAC and Europe display a more even spread across all three categories, pointing to diversified attack strategies. These variations suggest that attackers are not operating uniformly but are instead adapting campaigns to regional digital habits, payment ecosystems, and trust patterns – maximizing effectiveness by aligning phishing content with the most commonly used financial services in each market.

Distribution of financial phishing pages by category and region, 2025 (download)

Online shopping scams

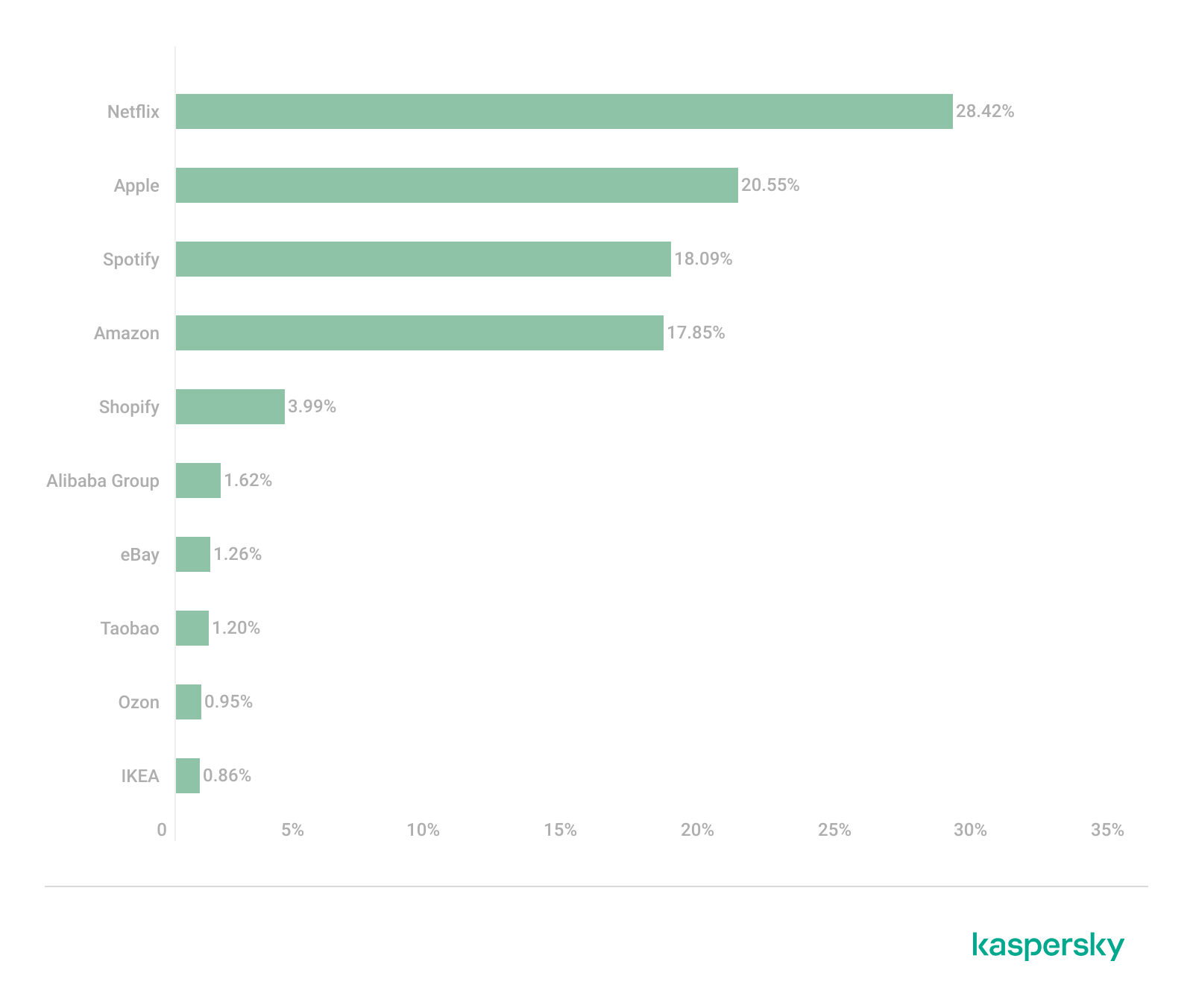

The distribution of organizations mimicked by phishing and scam pages in 2025 highlights a clear shift toward globally recognized digital service and e-commerce brands, with attackers prioritizing platforms that have large, active user bases and frequent payment interactions.

Netflix (28.42%) solidified its ranking as the most impersonated brand, followed by Apple (20.55%), Spotify (18.09%), and Amazon (17.85%). This reflects a move away from traditional retail-only targets toward subscription-based and ecosystem-driven services.

TOP 10 online shopping brands mimicked by phishing and scam pages, 2025 (download)

Regionally, this trend varies: Netflix dominates heavily in the Middle East, Apple leads in APAC, while Spotify ranks first across Europe, LATAM, and Africa. Although most of the top platforms are highly popular across different regions, we may suggest that the attackers tailor brand impersonation to regional popularity and user engagement.

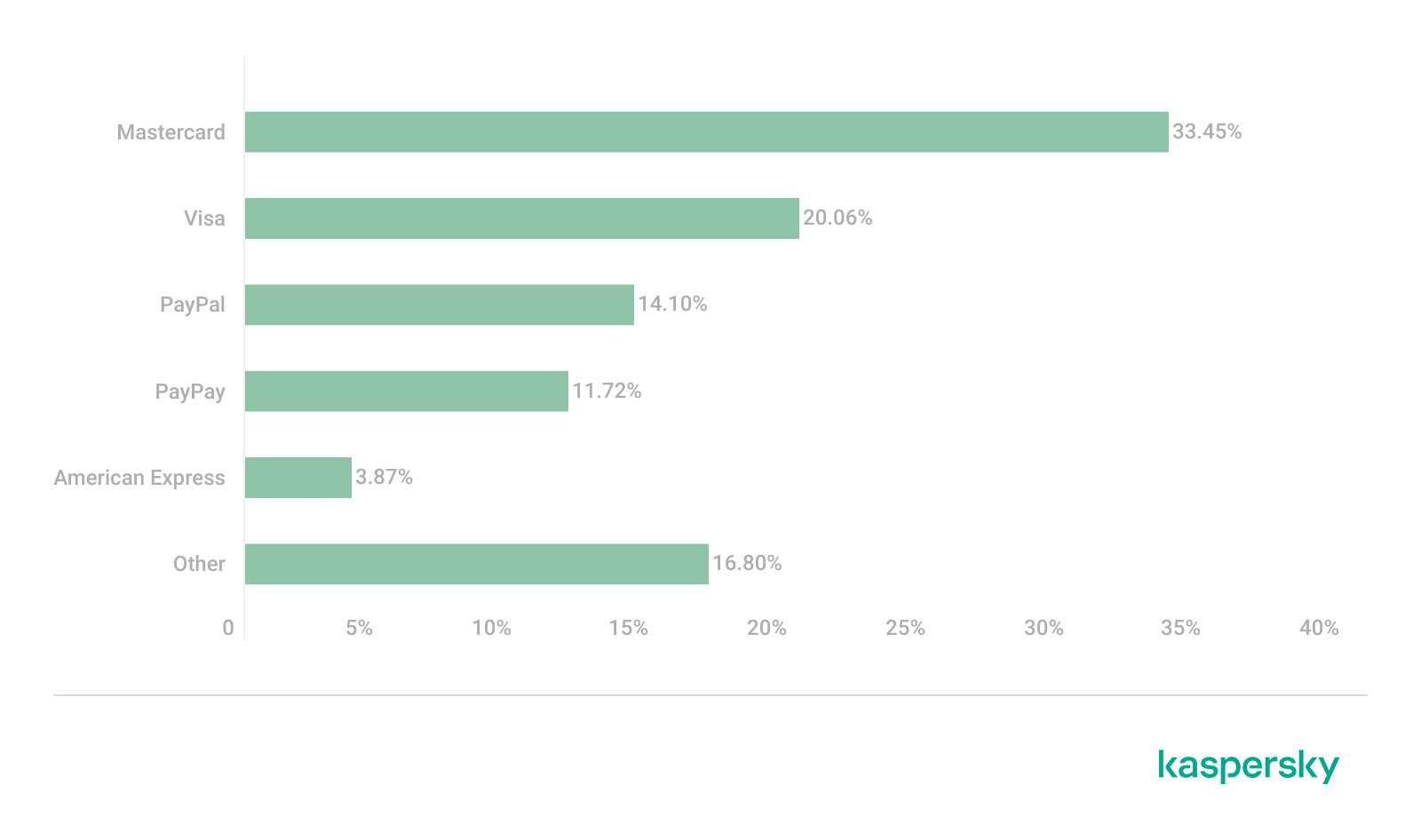

Payment system phishing

Phishing campaigns are impersonating multiple payment ecosystems to maximize coverage. While PayPal was the most mimicked in 2024 with 37.53%, its share dropped to 14.10% in 2025. Mastercard, on the contrary, attracted cybercriminals’ attention, its share increasing from 30.54% to 33.45%, while Visa accounted for a significant 20.06% (last year, it wasn’t in the TOP 5), reinforcing the growing focus on widely used banking card networks. The continued presence of American Express (3.87%) and the increasing number of pages mimicking PayPay (11.72%) further highlight attacker experimentation and regional adaptation.

TOP 5 payment systems mimicked by phishing and scam pages, 2025 (download)

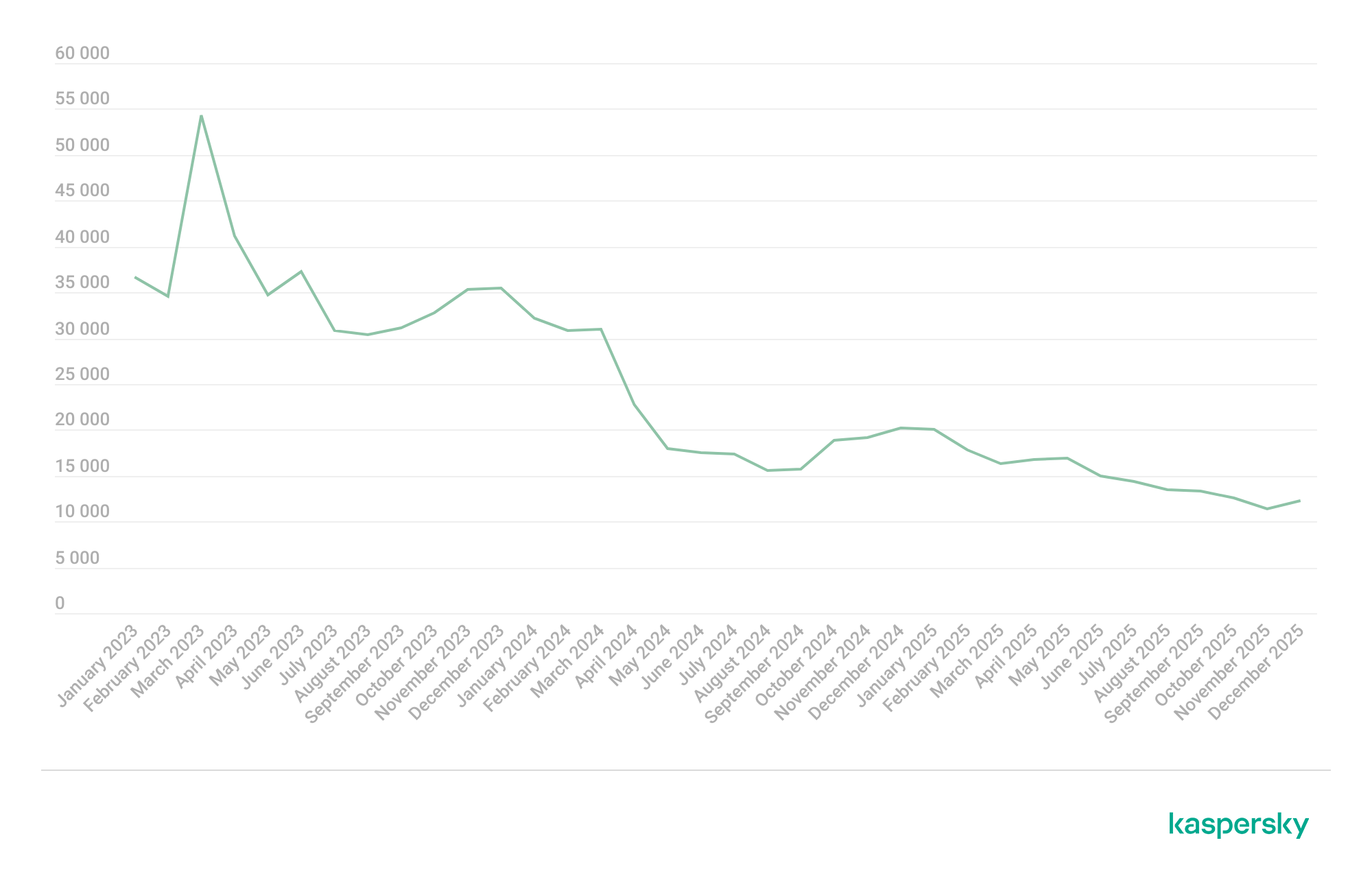

Financial malware

In 2025, the decline in users affected by financial PC malware continued. On the one hand, people continue to rely on mobile devices to manage their finances. On the other hand, some of the most prominent malware families that were initially designed as bankers had not used this functionality for years, so we excluded them from these statistics.

Changes in the number of unique users attacked by banking malware, by month, 2023–2025 (download)

Windows systems remained the primary platform targeted by attackers with financial malware. According to Kaspersky Security Bulletin, overall detections included 1,338,357 banking Trojan attacks globally from November 2024 to October 2025, though this number is also declining due to increasing focus on mobile vectors. Desktop threats continued to be distributed via traditional delivery methods like malicious emails, compromised websites, and droppers.

In 2025, Brazilian-origin families such as Grandoreiro (part of the Tetrade group) stood out for their constant activity and global reach. Despite a major law enforcement disruption in early 2024, Grandoreiro remained active in 2025, re-emerging with updated variants and continuing to operate. Other notable actors included Coyote and emerging families like Maverick, which abused WhatsApp for distribution while maintaining fileless techniques and overlaps with established Brazilian banking malware to steal credentials and enable fraudulent transactions on desktop banking platforms. Besides traditional bankers, other Brazilian malware families are worth mentioning, which specifically target relatively new and highly popular regional payment systems. One of the most prominent threats among these is GoPix Trojan focusing on the users of Brazilian Pix payment system. It is also capable of targeting local Boleto payment method, as well as stealing cryptocurrency.

There was also a surge in incidents in 2025 in which fraudsters targeted organizations through electronic document management (EDM) systems, for example, by substituting invoice details to trick victims into transferring funds. The Pure Trojan was most frequently encountered in such attacks. Attackers typically distribute it through targeted emails, using abbreviations of document names, software titles, or other accounting-related keywords in the headers of attached files. Globally in the corporate segment, Pure was detected 896 633 times over 2025, with over 64 thousand users attacked.

Contrary to PC banking malware, mobile banker attacks grew by 1.5 times in 2025 compared to the previous reporting period, which is consistent with their growth in 2024. They also saw a sharp surge in the number of unique installation packages. More statistics and trends on mobile banking malware can be found in our yearly mobile threat report.

Complementing traditional financial malware, infostealers played a significant role in enabling financial crime both on PCs and mobile devices by harvesting credentials, cookies, and autofill data from browsers and applications, which attackers then used for account takeovers or direct banking fraud. Kaspersky analyses pointed to a surge in infostealer detections (up by 59% globally on PCs), fueling credential-based attacks.

Financial cyberthreats on the dark web

The Kaspersky Digital Footprint Intelligence (DFI) team closely monitors infostealer activity on both PC and mobile devices to analyze emerging trends and assess the evolving tactics of cybercriminals.

Fraudsters especially target financial data such as payment cards, cryptocurrency wallets, login credentials and cookies for banking services, as well as documents stored on the victim’s device. The stolen data is collected in log files and shared on dark web resources, where they are bought, sold, or distributed freely and then used for financial fraud.

With access to financial data, fraudsters can gain control of users’ bank accounts and payment cards, and withdraw funds. Compromised accounts and cards are also frequently used in subsequent activities, turning the victims into intermediaries in a fraud scheme.

Compromised accounts

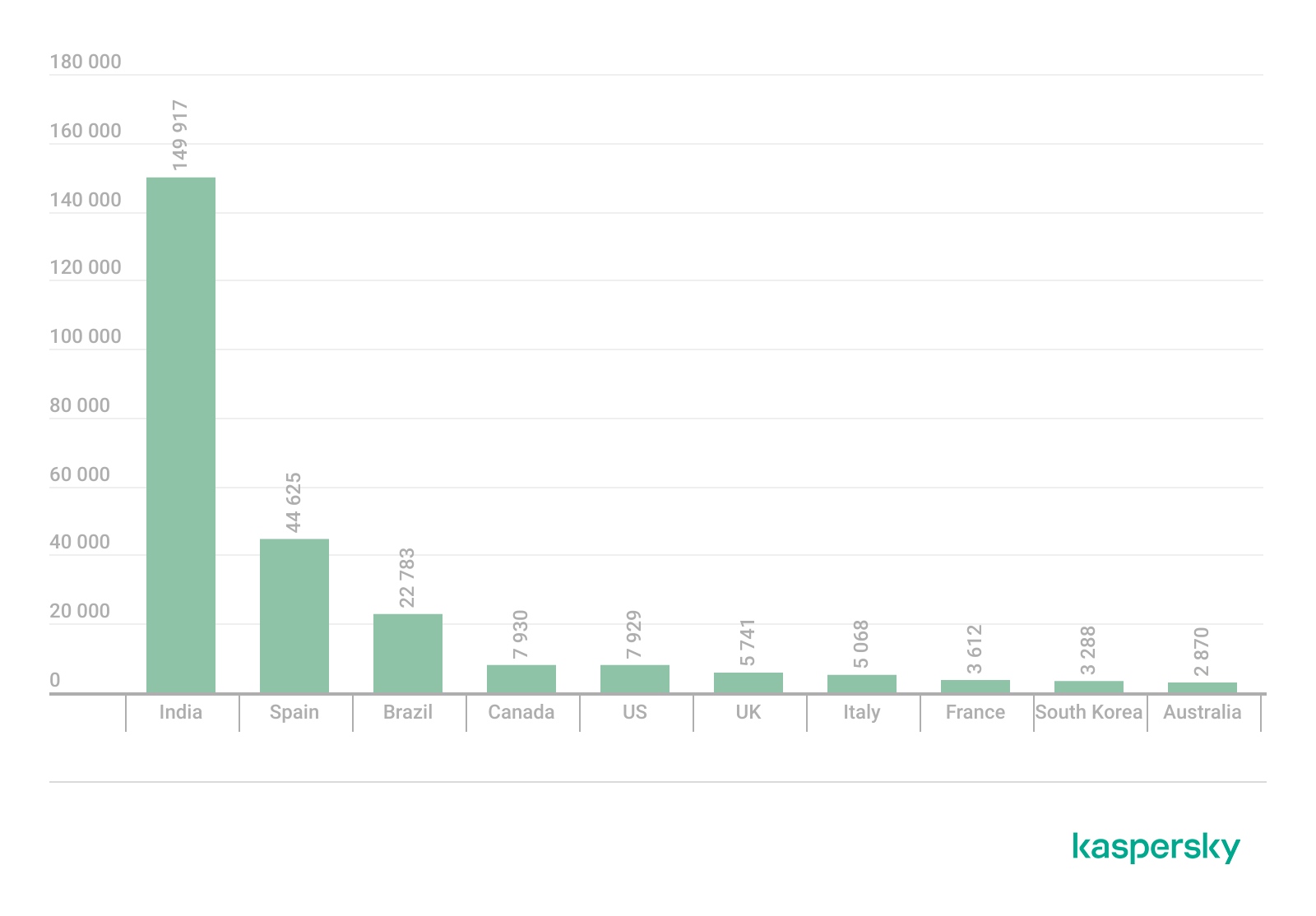

Kaspersky DFI found that in 2025, over one million online banking accounts (these are not Kaspersky product users) served by the world’s 100 largest banks fell victim to infostealers: their credentials were being freely shared on the dark web.

The countries with the highest median number of compromised accounts per bank were India, Spain, and Brazil.

The chart below shows the median number of compromised accounts per bank for the TOP 10 countries.

TOP 10 countries with the highest compromised account median (download)

Compromised payment cards

Seventy-four percent of payment cards that were compromised by infostealer malware, published on dark web resources and identified by the Digital Footprint Intelligence team in 2025, remained valid as of March 2026. This means that attackers could still use the cards that had been stolen months or even years prior.

It should be noted that the number of bank accounts and payment cards known to have been compromised by infostealers in 2025 will continue to rise, because fraudsters do not publish the log files immediately after the compromise but only after a delay of months or even years.

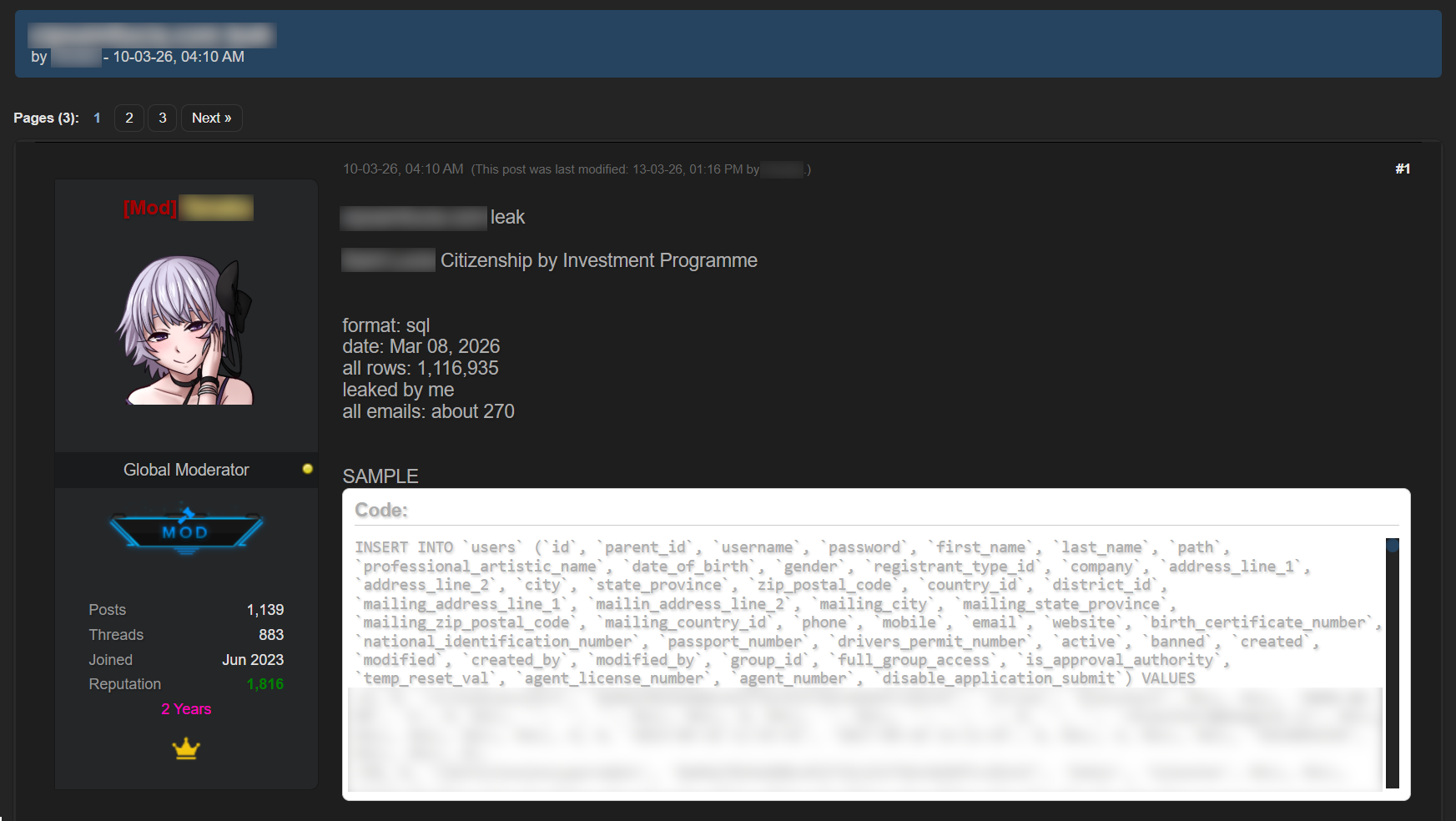

Data breaches

Regardless of the industry in which the target company operates, data breaches often expose users’ financial data, including payment card information, bank account details, transaction histories and other financial information. As a consequence, the compromised databases are sold and distributed on underground resources.

It should be noted that the threat is not limited to the exposure of financial information alone. Various identity documents and even seemingly public data, such as names, phone numbers and email addresses, can become a risk when they are published on the dark web. Such data attracts fraudsters’ attention and can be used in social engineering attacks to gain access to the user’s financial assets.

An example of a post offering a database

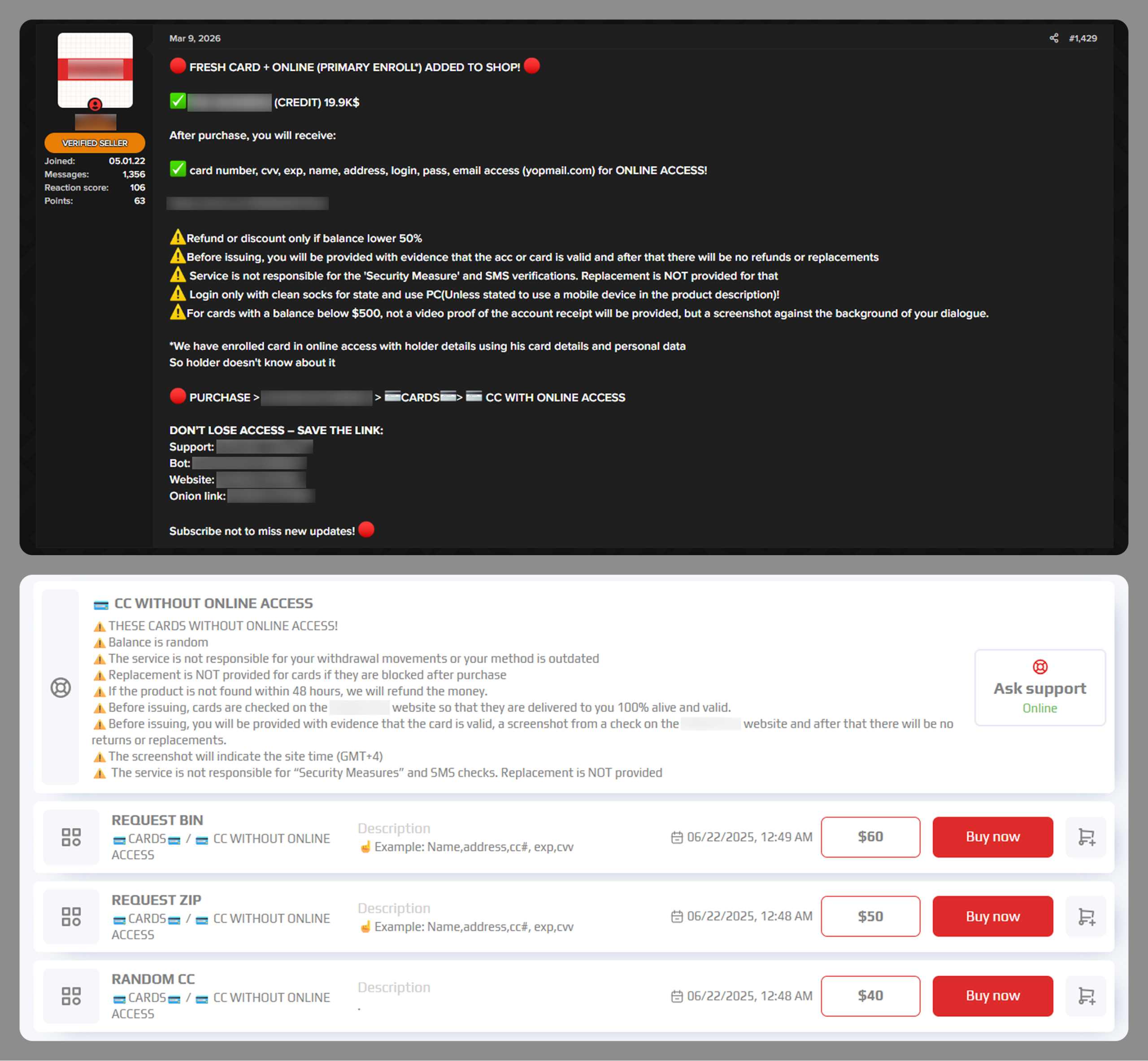

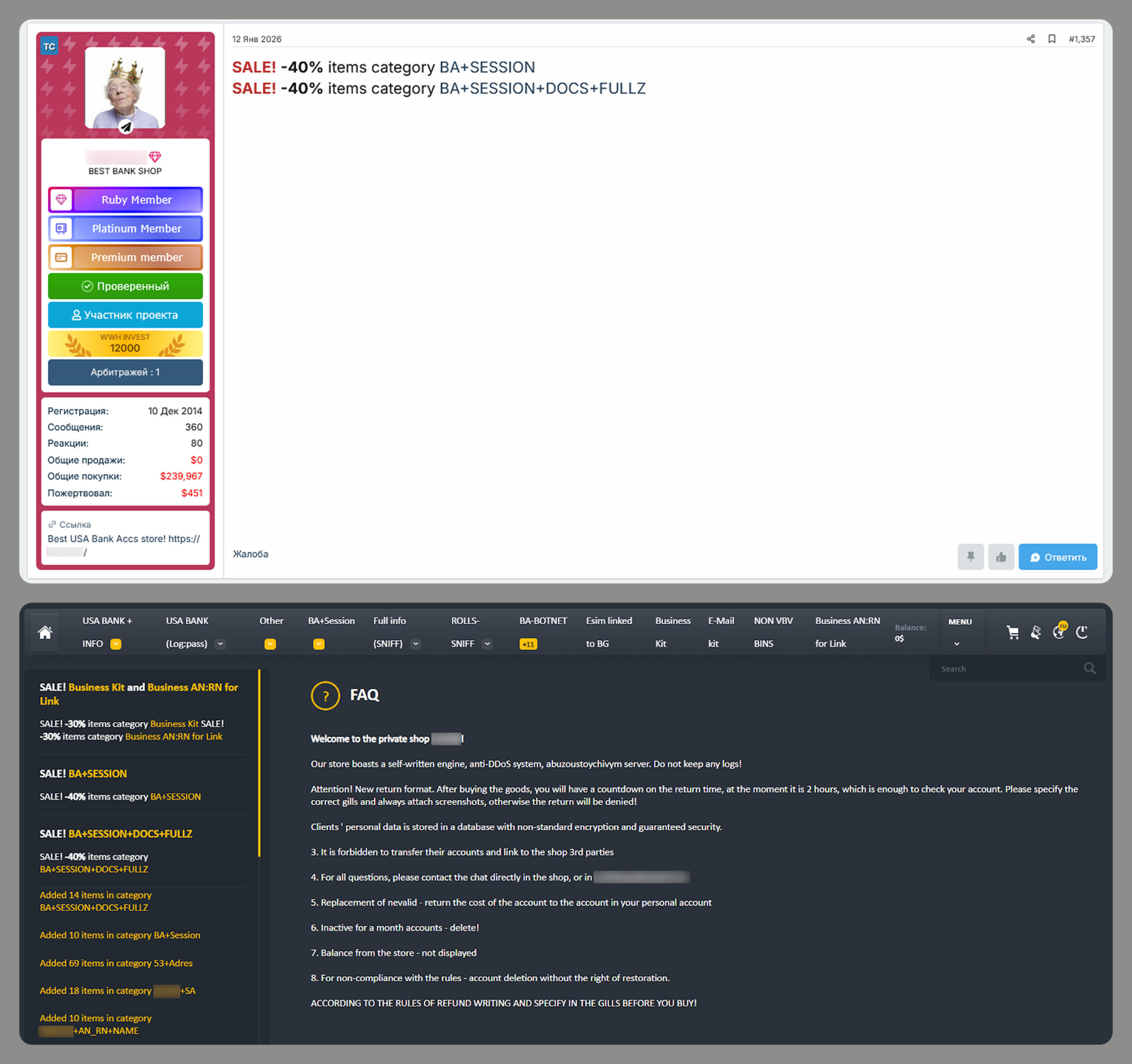

Sale of bank accounts and payment cards

The dark web often features services provided by stores that specialize in selling bank accounts and payment cards. Fraudsters typically obtain data for sale from a variety of sources, including infostealer logs and leaked databases, which are first repackaged and then combined.

Examples of a post (top) and a site (bottom) offering payment cards

Often, sellers offer complete victim profiles, referred to by fraudsters as “fullz”. These include not only bank accounts or payment cards but also identification documents, dates of birth, residential addresses, and other personal details. A full‑information package is usually more expensive than a payment card or a bank account alone.

Examples of a post (top) and a site (bottom) offering bank accounts

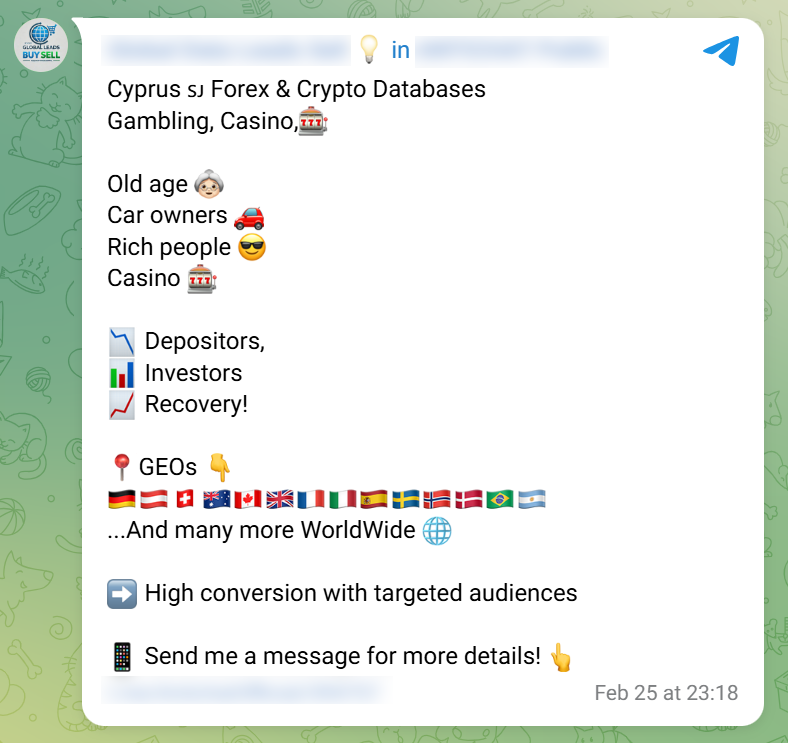

Compiled databases

Fraudsters exploit various sources, including previously leaked databases, to compile new, thematic ones. Finance- and, in particular, cryptocurrency-related databases, are among the most popular. Compilations aimed at specific user groups, such as the elderly or wealthy people, are also of interest to cybercriminals.

Usually, thematic databases contain personal information about users, such as names, phone numbers, and email addresses. Fraudsters can use this data to launch social engineering attacks.

An example of a message offering compiled databases

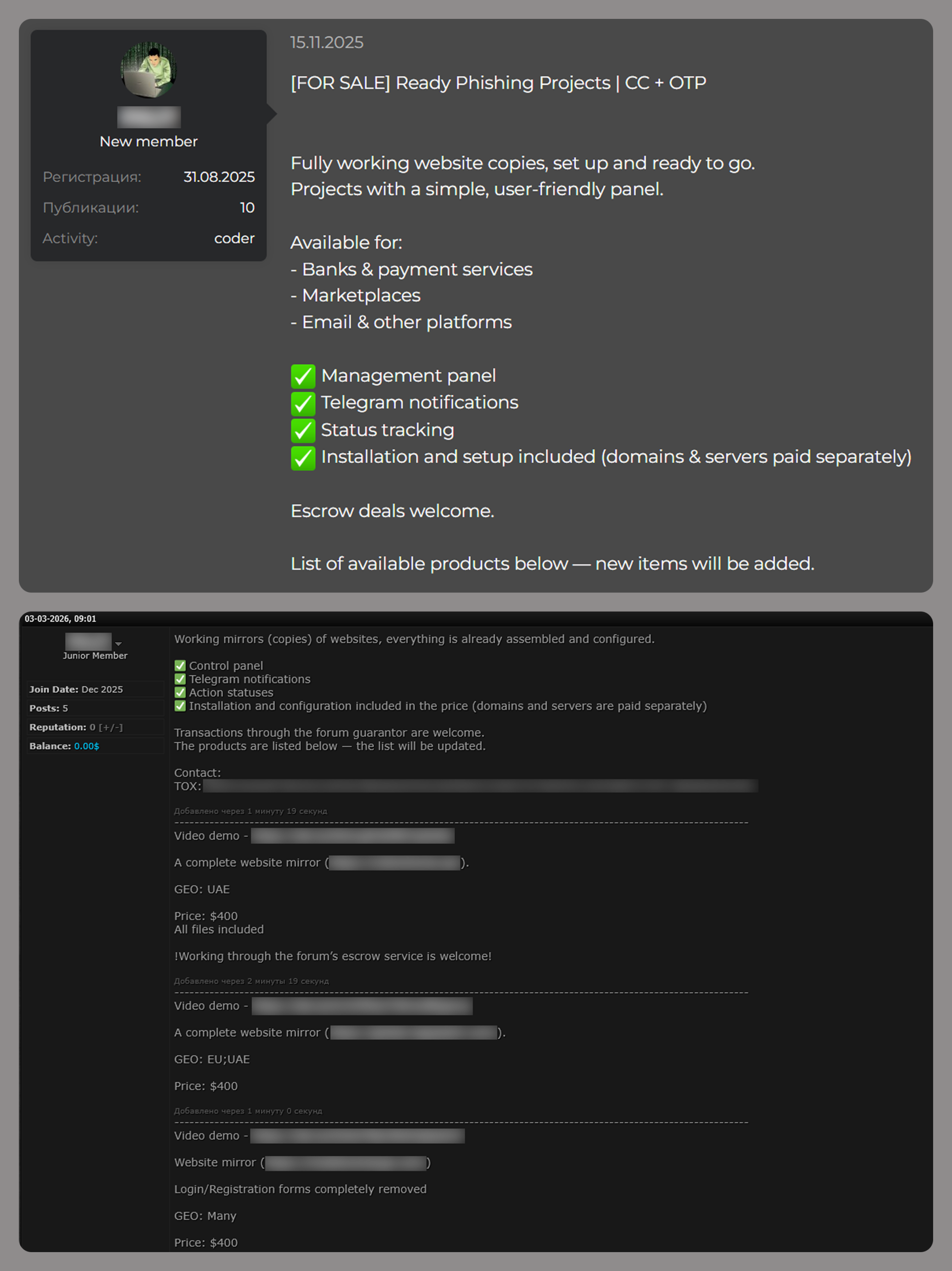

Creation of phishing websites

Phishing websites have become a powerful tool for the financial enrichment of fraudsters. Cybercriminals create fraudulent sites that masquerade as legitimate resources of companies operating in various industries. Gambling and retail sites remain among the most popular targets.

In order to obtain personal and financial information from unsuspecting users, adversaries seek out ways to create such phishing websites. Ready-made layouts and website copies are sold on the dark web and advertised as profitable tools. Moreover, fraudsters offer phishing website creation services.

Examples of posts offering creation of phishing websites

Conclusion

The decline of traditional PC banking malware is not an indicator of reduced risk; rather, it highlights a redistribution of attacker effort toward more efficient methods targeting mobile devices, credential theft, and social engineering. Infostealers, in particular, are a force multiplier, enabling widespread compromise at scale.

Looking ahead to 2026, the financial threat landscape is expected to become even more data-driven and automated. Organizations must adapt by focusing on identity protection, real-time monitoring, and cross-channel threat intelligence, while users must remain vigilant against increasingly sophisticated and personalized attack techniques.

AI tool Vercel was abused by cybercriminals to create a Malwarebytes lookalike website.

Cybercriminals no longer need design or coding skills to create a convincing fake brand site. All they need is a domain name and an AI website builder. In minutes, they can clone a site’s look and feel, plug in payment or credential-stealing flows, and start luring victims through search, social media, and spam.

One side effect of being an established and trusted brand is that you attract copycats who want a slice of that trust without doing any of the work. Cybercriminals have always known it is much easier to trick users by impersonating something they already recognize than by inventing something new—and developments in AI have made it trivial for scammers to create convincing fake sites.

Registering a plausible-looking domain is cheap and fast, especially through registrars and resellers that do little or no upfront vetting. Once attackers have a name that looks close enough to the real thing, they can use AI-powered tools to copy layouts, colors, and branding elements, and generate product pages, sign-up flows, and FAQs that look “on brand.”

Over a three‑month period leading into the 2025 shopping season, researchers observed more than 18,000 holiday‑themed domains with lures like “Christmas,” “Black Friday,” and “Flash Sale,” with at least 750 confirmed as malicious and many more still under investigation. In the same window, about 19,000 additional domains were registered explicitly to impersonate major retail brands, nearly 3,000 of which were already hosting phishing pages or fraudulent storefronts.

These sites are used for everything from credential harvesting and payment fraud to malware delivery disguised as “order trackers” or “security updates.”

Attackers then boost visibility using SEO poisoning, ad abuse, and comment spam, nudging their lookalike sites into search results and promoting them in social feeds right next to the legitimate ones. From a user’s perspective, especially on mobile without the hover function, that fake site can be only a typo or a tap away.

When the impersonation hits home

A recent example shows how low the barrier to entry has become.

We were alerted to a site at installmalwarebytes[.]org that masqueraded from logo to layout as a genuine Malwarebytes site.

Close inspection revealed that the HTML carried a meta tag value pointing to v0 by Vercel, an AI-assisted app and website builder.

The tool lets users paste an existing URL into a prompt to automatically recreate its layout, styling, and structure—producing a near‑perfect clone of a site in very little time.

The history of the imposter domain tells an incremental evolution into abuse.

Registered in 2019, the site did not initially contain any Malwarebytes branding. In 2022, the operator began layering in Malwarebytes branding while publishing Indonesian‑language security content. This likely helped with search reputation while normalizing the brand look to visitors. Later, the site went blank, with no public archive records for 2025, only to resurface as a full-on clone backed by AI‑assisted tooling.

Traffic did not arrive by accident. Links to the site appeared in comment spam and injected links on unrelated websites, giving users the impression of organic references and driving them toward the fake download pages.

Payment flows were equally opaque. The fake site used PayPal for payments, but the integration hid the merchant’s name and logo from the user-facing confirmation screens, leaving only the buyer’s own details visible. That allowed the criminals to accept money while revealing as little about themselves as possible.

Behind the scenes, historical registration data pointed to an origin in India and to a hosting IP (209.99.40[.]222) associated with domain parking and other dubious uses rather than normal production hosting.

Combined with the AI‑powered cloning and the evasive payment configuration, it painted a picture of low‑effort, high‑confidence fraud.

AI website builders as force multipliers

The installmalwarebytes[.]org case is not an isolated misuse of AI‑assisted builders. It fits into a broader pattern of attackers using generative tools to create and host phishing sites at scale.

Threat intelligence teams have documented abuse of Vercel’s v0 platform to generate fully functional phishing pages that impersonate sign‑in portals for a variety of brands, including identity providers and cloud services, all from simple text prompts. Once the AI produces a clone, criminals can tweak a few links to point to their own credential‑stealing backends and go live in minutes.

Research into AI’s role in modern phishing shows that attackers are leaning heavily on website generators, writing assistants, and chatbots to streamline the entire kill chain—from crafting persuasive copy in multiple languages to spinning up responsive pages that render cleanly across devices. One analysis of AI‑assisted phishing campaigns found that roughly 40% of observed abuse involved website generation services, 30% involved AI writing tools, and about 11% leveraged chatbots, often in combination. This stack lets even low‑skilled actors produce professional-looking scams that used to require specialized skills or paid kits.

Growth first, guardrails later

The core problem is not that AI can build websites. It’s that the incentives around AI platform development are skewed. Vendors are under intense pressure to ship new capabilities, grow user bases, and capture market share, and that pressure often runs ahead of serious investment in abuse prevention.

As Malwarebytes General Manager Mark Beare put it:

“AI-powered website builders like Lovable and Vercel have dramatically lowered the barrier for launching polished sites in minutes. While these platforms include baseline security controls, their core focus is speed, ease of use, and growth—not preventing brand impersonation at scale. That imbalance creates an opportunity for bad actors to move faster than defenses, spinning up convincing fake brands before victims or companies can react.”

Site generators allow cloned branding of well‑known companies with no verification, publishing flows skip identity checks, and moderation either fails quietly or only reacts after an abuse report. Some builders let anyone spin up and publish a site without even confirming an email address, making it easy to burn through accounts as soon as one is flagged or taken down.

To be fair, there are signs that some providers are starting to respond by blocking specific phishing campaigns after disclosure or by adding limited brand-protection controls. But these are often reactive fixes applied after the damage is done.

Meanwhile, attackers can move to open‑source clones or lightly modified forks of the same tools hosted elsewhere, where there may be no meaningful content moderation at all.

In practice, the net effect is that AI companies benefit from the growth and experimentation that comes with permissive tooling, while the consequences is left to victims and defenders.

We have blocked the domain in our web protection module and requested a domain and vendor takedown.

How to stay safe

End users cannot fix misaligned AI incentives, but they can make life harder for brand impersonators. Even when a cloned website looks convincing, there are red flags to watch for:

Before completing any payment, always review the “Pay to” details or transaction summary. If no merchant is named, back out and treat the site as suspicious.

Do not follow links posted in comments, on social media, or unsolicited emails to buy a product. Always follow a verified and trusted method to reach the vendor.

If you come across a fake Malwarebytes website, please let us know.

We don’t just report on threats—we help safeguard your entire digital identity

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}